Risks and opportunities are key external and internal variables that have a positive or

negative influence on a company’s business model and its ability to create value (both

financial and non-financial). A company does not operate in a vacuum. Its operations,

products, and services have a positive or negative impact on its surrounding environment,

employees, and clients, and the communities in which it operates.

Reporting on risks, impacts, and opportunities and how a company manages them helps

investors and other stakeholders understand whether the company can address future

challenges, reduce its impact, and realize opportunities.

According to International Financial Reporting Standards (IFRS) S1, a company must disclose about all material sustainability-related risks and opportunities. Other IFRS Sustainability Disclosure Standards specify what companies must disclose about specific sustainability-related risks and opportunities (IFRS S2 on Climate-related Disclosures). In addition, companies must refer to and consider the applicability of disclosures in the industry-based Sustainable Accounting Standards Board (SASB) standards for specific sectors.

A company may also consider:

- The Climate Disclosure Standards Board CDSB Framework Application Guidance for Water-Related Disclosures and the CDSB Framework Application Guidance for

Biodiversity-related Disclosures. - The most recent work of other standard setters whose requirements are also

designed to meet investors’ information needs. - The sustainability-related risks and opportunities identified by other companies in

the same industry or region as the reporting company.

Learn more about sustainability-related risks and opportunities:

In the Global Reporting Initiative (GRI) standards, “impact” is the effect an organization has or could have on the economy, environment, and people, including effects on their human rights as a result of the organization’s activities or business relationships. The impacts can be actual or potential, negative or positive, short-term or long-term, intended or unintended, and reversible or irreversible. The impacts indicate the organization’s positive or negative contribution to sustainable development.

The impacts on the economy, environment, and people are interrelated—for example, an organization’s impacts on the economy and environment can result in impacts on people and their human rights. Similarly, an organization’s positive impacts can result in negative impacts and vice versa—for example, an organization's positive impacts on the environment can lead to negative impacts on people and their human rights (GRI 1: Foundation 2021, Section 2.1).

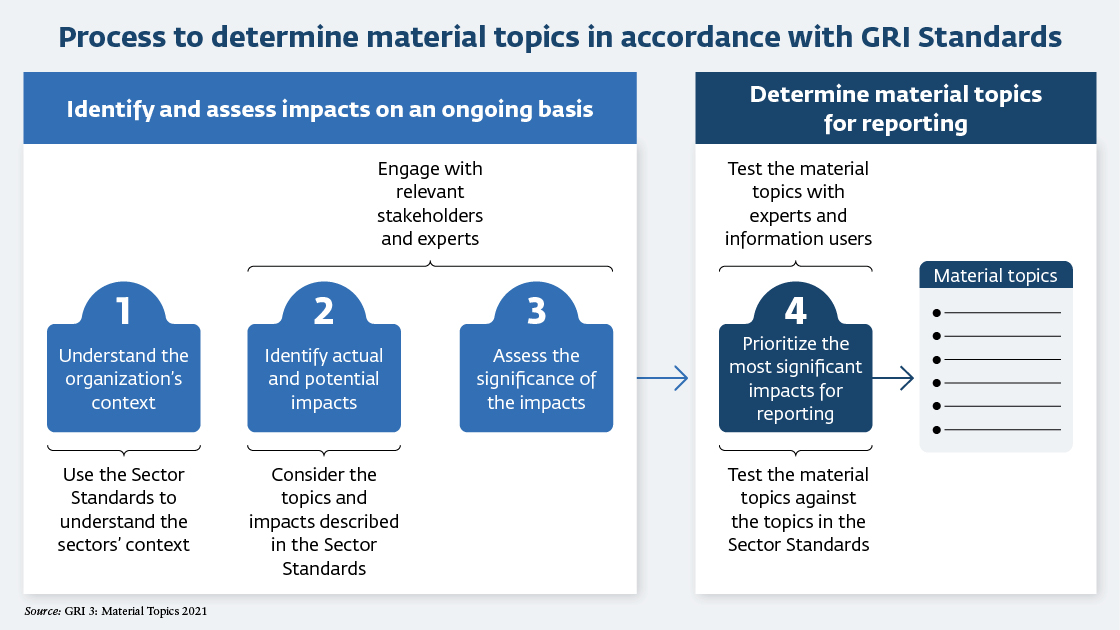

An organization reporting in accordance with the GRI standards is required to determine its material topics using the applicable GRI sector standards (see GRI 1: Foundation 2021, requirement 3 and box 5).

GRI 3: Material Topics describes the four steps that the organization should follow in determining its material topics (see figure 1). Following these steps helps the organization determine its material topics and disclose them The steps provide guidance but are not requirements on their own.

Figure 1. Four Steps to Determining Material Topic

Learn more about sustainability-related impacts: