Understanding the Global Reporting Frameworks

There is growing investor interest in companies engaged in sustainable business activities. Investors want to understand how companies tackle issues such as climate change, gender diversity, or supply chain risks that may have a material impact on their business.

Stock exchanges and regulators develop sustainability and climate disclosure regulations. Currently, 71 - more than half of stock exchanges worldwide have guidance on ESG disclosure; in 2015, it was only 13. Mandatory rules are in 27 markets, of which 16 are emerging markets, according to the UN Sustainability Stock Exchanges database.

Harmonizing sustainability disclosure standards will create reliable and comparable ESG data and disclosures, which is increasingly critical to attract capital and investors and prevent greenwashing.

A welcoming step in the convergence of different standards and frameworks are the new sustainability and climate-reporting standards by the IFRS Foundation and the European Sustainability Reporting Standards.

IFRS Sustainability Disclosure standards were finalized in June 2023 and took effect from January 2024, and the European Sustainability Reporting Standards were launched in July 2023, effective as of January 2024.

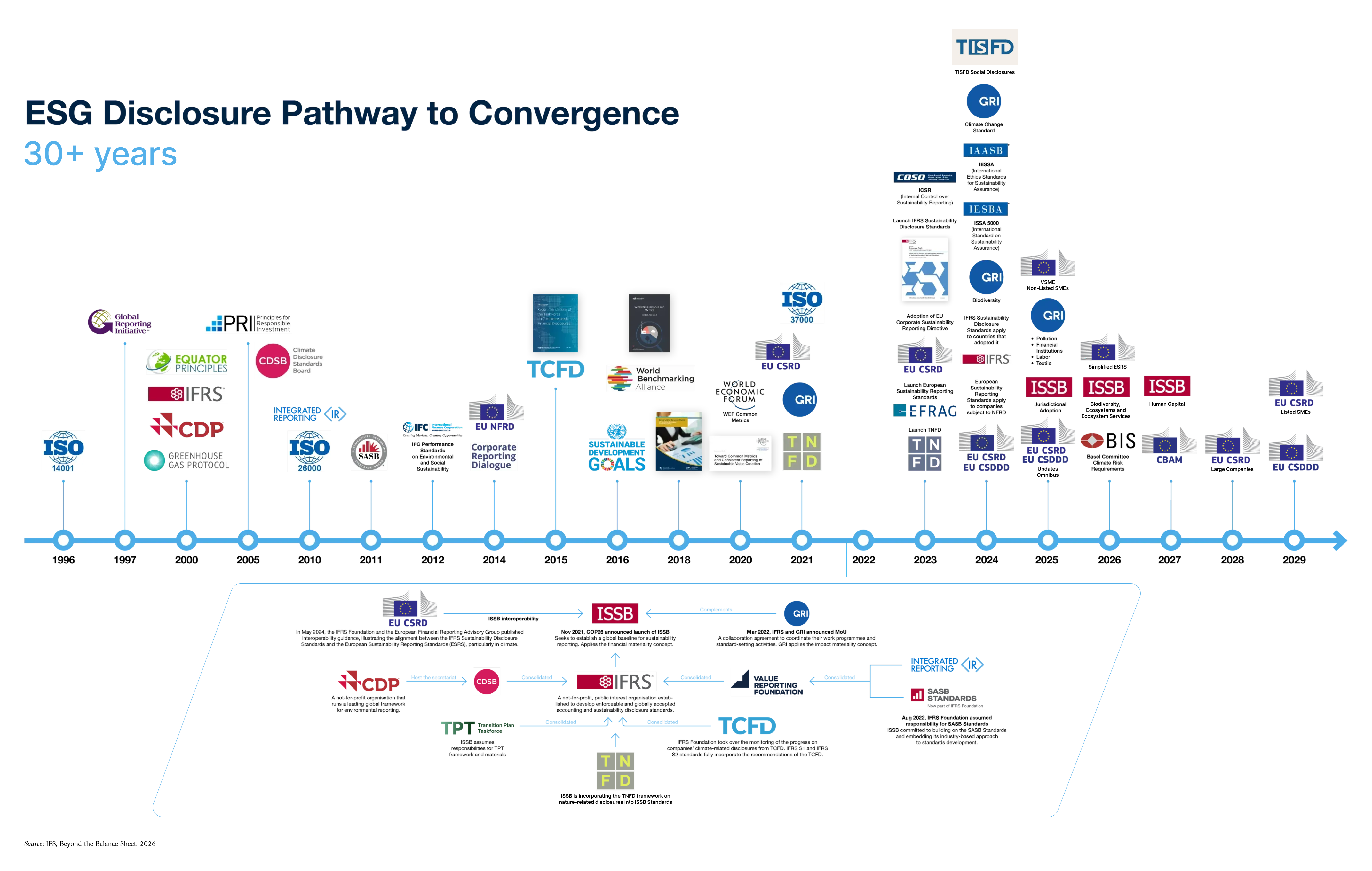

The diagram below presents the key milestone in sustainability disclosure going mainstream over the last 30 plus years.

Source: IFC, 2026

-

IFRS Sustainability Disclosure Standards

The IFRS Sustainability Disclosure Standards are developed by the International Sustainability Standards Board (ISSB). The ISSB is an independent, private-sector body that develops – in the public interest – standards that will result in a high-quality, comprehensive global baseline of sustainability disclosures focused on the needs of investors and the financial markets.

The ISSB's standards focus on sustainability-relayed risks and opportunities that are material for investors and are largely build on the Task Force for Climate-related Financial Information (TCFD) Recommendations (see below). As such, implementing the IFRS Sustainability Disclosure Standards also fulfills means that a company has implemented the TCFD Recommendations. The standards cover four core content areas

- Governance: the governance processes, controls and procedures the entity uses to monitor and manage sustainability-related risks and opportunities

- Strategy: the approach the entity uses to manage sustainability-related risks and opportunities

- Risk Management: the processes the entity uses to identify, assess, prioritize and monitor sustainability-related risks and opportunities

- Metrics and Targets: the entity’s performance in relation to sustainability-related risks and opportunities, including progress towards any targets the entity has set or is required to meet by law or regulation

IFRS S1 General Requirements for Disclosure of Sustainability-Related Financial Information provides the conceptual foundations and disclosure content for reporting all sustainability-related financial information, while IFRS S2 Climate-Related Disclosures provides more detailed requirements focusing on climate-related risks and opportunities, within the foundations of IFRS S1. Companies must consider the applicability of the industry-based Sustainability Accounting Standards Board (SASB) Standards (see below) when applying the IFRS Sustainability Disclosure Standards. The standards are to be applied as of January 1, 2024.

Given that IFRS S2 requires information on transition plans to be disclosed (where an entity has such a plan) and that transition plans are a growing component of corporate climate-related disclosures, the ISSB announced that it will assume responsibility for the disclosure-specific materials developed by the Transition Plan Taskforce. Potentially building on pre-existing initiatives, including the SASB standards, CDSB guidance, and the work of the Task Force on Nature-related Financial Disclosures, the ISSB also decided to look into risks and opportunities associated with biodiversity and human capital in the coming two years.

Designed for mandatory adoption by regulators, the IFRS Sustainability Disclosure Standards are being gradually implemented into reporting requirements around the world.

-

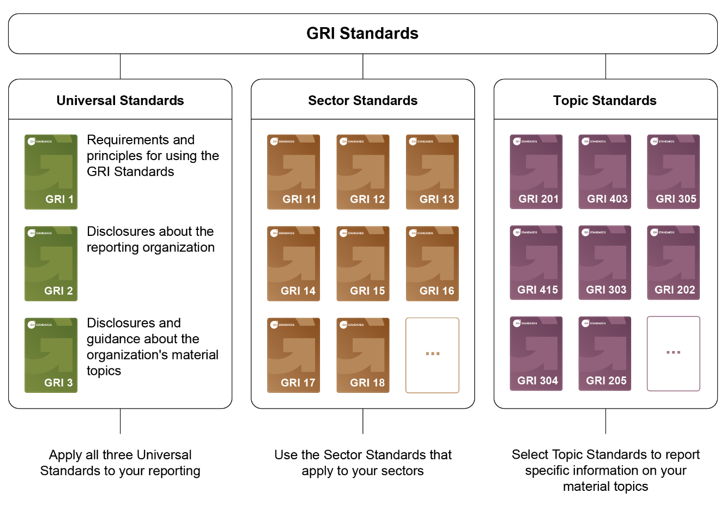

Global Reporting Initiative (GRI) Standards

The GRI Standards represent global best practice for reporting publicly on a range of economic, environmental and social impacts. Sustainability reporting based on the Standards provides information about an organization’s positive or negative contributions to sustainable development.

The GRI Standards is a modular system of interconnected standards, delivering an inclusive picture of an organization's material topics, their related impacts, and how they are managed. Three series of Standards support the reporting process:

- the GRI Universal Standards, which apply to all organizations;

- the GRI Sector Standards, applicable to specific sectors;

- the GRI Topic Standards, each listing disclosures relevant to a particular topic.

Using these Standards helps organizations to determine what topics are most to achieve sustainable development.

Source: GRI -

European Sustainability Reporting Standards

The EU Corporate Sustainability Reporting Directive (CSRD) modernizes and strengthens the rules concerning the social and environmental information that companies headquartered in the EU, or those with significant operations in the EU, have to report. A broader set of large companies, as well as listed SMEs, will now be required to report on sustainability.

Certain European companies have to apply the new rules from the 2024 financial year, for reports published in 2025, with others being phased in over 2026 and 2027. Finally, non-EU companies with significant operations in Europe will have to start reporting from 2029, based on FY 2028 data, using a simplified set of standards.

Companies subject to the CSRD will have to report according to European Sustainability Reporting Standards (ESRS).

The ESRS set general requirements for to guide the disclosure of all sustainability information and require all organizations to report on four areas of general disclosures:

- Governance

- Strategy

- Impacts, risks, and opportunities

- Metrics and targets

Depending on their materiality to the organization, it may also disclose using a number of topical standards:

Environmental

- Climate Change

- Pollution

- Water and marine resources

- Biodiversity and ecosystems

- Resource use and circular economy

Social

Governance

-

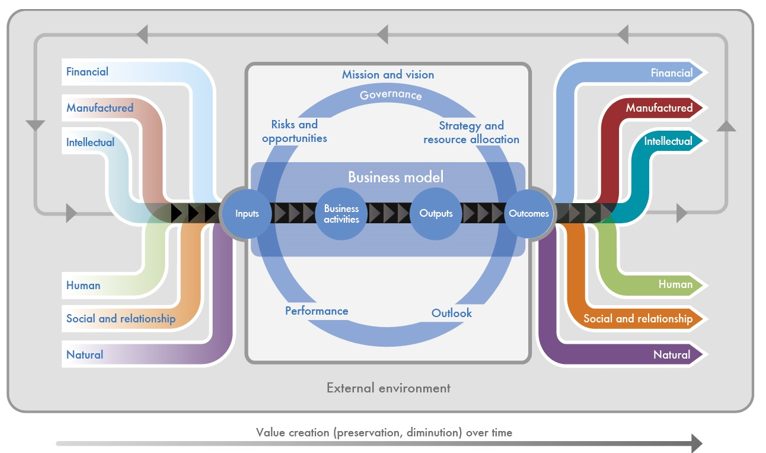

Integrated Reporting Framework (part of the IFRS Foundation)

The Integrated Reporting Framework is a principles-based framework used by organizations to communicate clearly and concisely about how its strategy, governance, performance and prospects – in the context of its external environment – lead to the creation, preservation or erosion of value over time. The Integrated Reporting Framework categorizes the inputs and outcomes of accompany into six capitals: Financial, Manufactured, Intellectual, Human, Social and relationship, and Natural.

As of August 2022, the International Sustainability Standards Board (ISSB) of the IFRS Foundation assumed responsibility for the Integrated Reporting Framework.

-

SASB Standards (part of the IFRS Foundation)

The SASB Standards help companies disclose material, industry-specific sustainability information to their investors in the context of the IFRS Sustainability Disclosure Standards (see above).

Available for 77 industries, the SASB Standards identify the sustainability-related risks and opportunities most likely to affect an entity’s cash flows, access to finance and cost of capital over the short, medium or long term and the disclosure topics and metrics that are most likely to be useful to investors.

As of August 2022, the International Sustainability Standards Board (ISSB) of the IFRS Foundation assumed responsibility for the SASB Standards. The ISSB has committed to maintain, enhance and evolve the SASB Standards and encourage their use, and in 2023 updated the standards to ensure their international applicability.

-

US SEC Climate Disclosure Rules

The US Securities and Exchange Commission has adopted new rules on climate-related disclosures in March 2024. These rules apply to all companies that have an existing requirement to report to the SEC, including, non-US companies that trade shares on a US exchange.

Built on the TCFD Recommendations (see below), the disclosure rules will require SEC registrants to disclose information on:

- Material climate-related risks

- Material impacts of climate-related risks on the organization’s strategy, business model and outlook

- Any climate risk mitigation or adaptation activities undertaken by the registrant, if applicable

- A description of the registrant’s climate transition plan, if applicable

- The material climate-related outcomes of a scenario analysis, if applicable

- The use of an internal carbon price by the registrant, if material

- Oversight of climate-related risks by the registrant’s board of directors and management

- Climate risk management processes, if applicable

- Climate related targets and goals, if applicable and material

- Material Scope 1 and/or Scope 2 emissions metrics, if the company is not exempted

- Certain financial maters related to materialized climate risk

The phased implementation, with a subset of registrants required to report a subset of the rules starting for their fiscal year beginning in 2025, until full implementation for reports covering fiscal year beginning 2027

A summary of the requirements is available here.

-

Task Force on Climate-related Financial Disclosures (TCFD) Recommendations (part of the IFRS Foundation)

The recommendations of the Task Force for Climate-Related Financial Disclosure (TCFD) were launched in 2017 “to help identify the information needed by investors, lenders, and insurance underwriters to appropriately assess and price climate-related risks and opportunities.” The TCFD Recommendations comprise of four core elements:

- Governance

- Strategy

- Risk Management

- Metrics and Targets

The recommendations were intended for voluntary implementation, but they are increasingly becoming mandatory in markets such as Brazil, Japan, Singapore, Switzerland, the United Kingdom, and others. More than 4,900 companies provided TCFD reports as of October 2023.

The climate-related and general sustainability-related disclosure standard of the International Sustainability Standards Board (ISSB) ) marked the culmination of the TCFD and the ISSB has now taken over responsibility for monitoring progress of companies’ climate-related disclosures from the TCFD.

For additional resources on TCFD, visit the TCFD Knowledge Hub, see the TCFD’s final status report and the TCFD publications web page.

{kind=link}

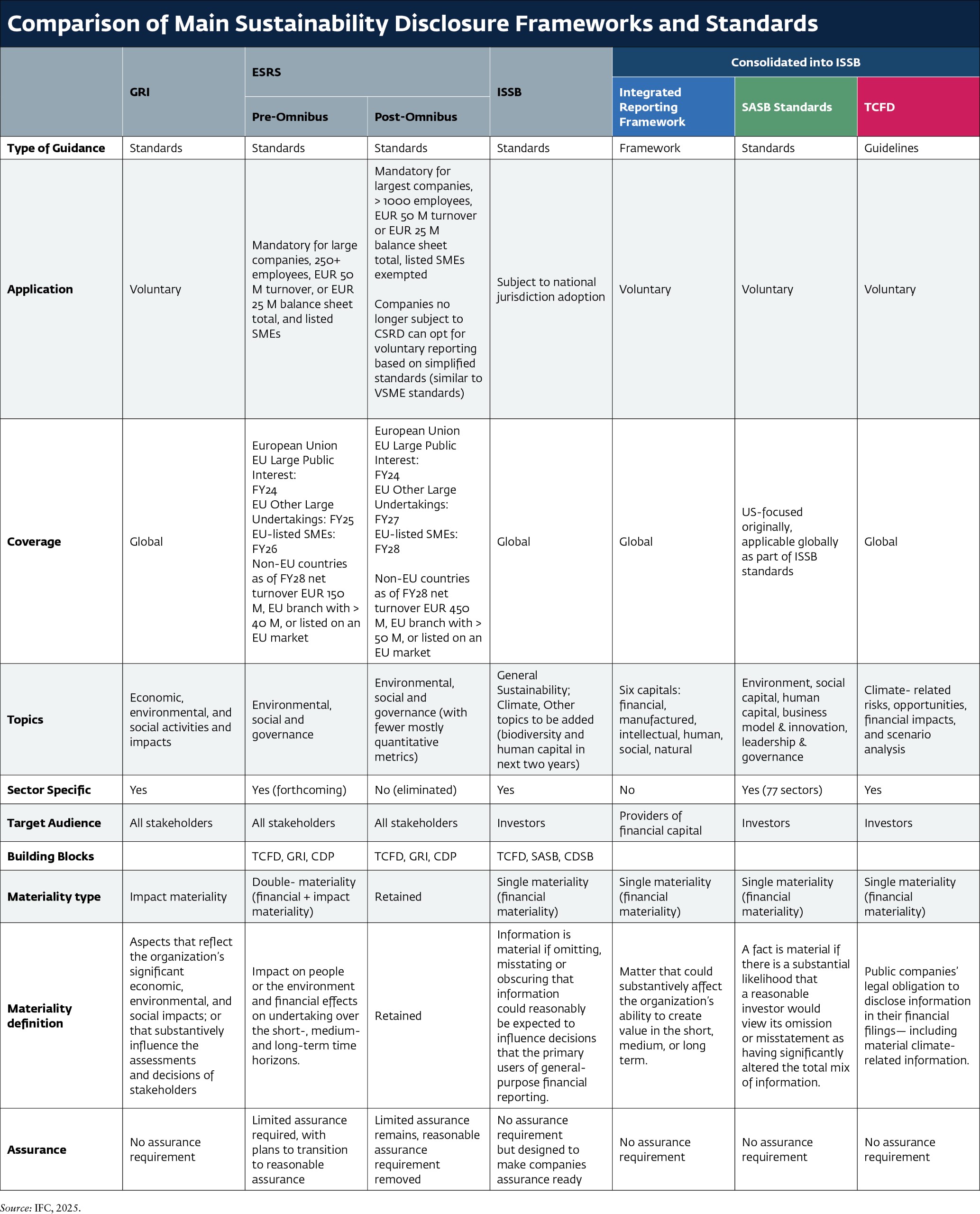

Comparing sustainability reporting standards and frameworks

The table below provides a summary comparison of the major sustainability frameworks and standards, including:

- International Sustainability Standards Board (ISSB) - IFRS S1 General Requirements for Disclosure of Sustainability-Related Financial Information and IFRS S2 Climate-related Disclosures;

- European Financial Reporting Advisory Group (EFRAG) - European Sustainability Reporting Standards;

- Global Reporting Initiative (GRI) Standards;

- Integrated Reporting Framework - Now part of IFRS Foundation;

- Sustainability Accounting Standards Board (SASB) - SASB Standards - Now part of IFRS Foundation;

- Task Force on Climate-related Financial Disclosures (TCFD) Recommendations - Now part of IFRS Foundation;

For resources on the IFRS Sustainability Disclosure Standards, check the ISSB Knowledge Hub.

For resources on the European Sustainability Reporting Standards, check the EFRAG ESRS Q&A Platform.

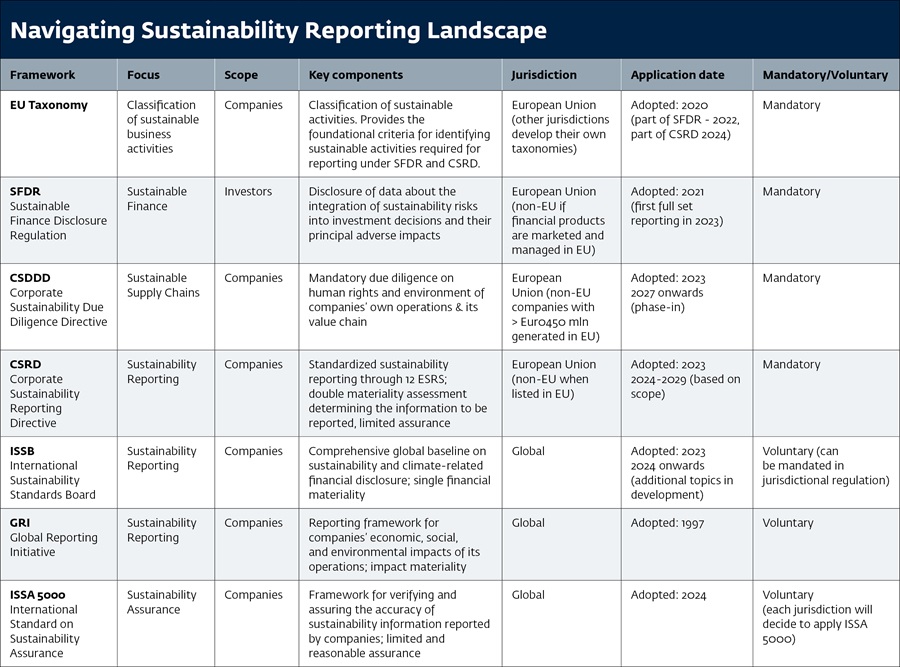

The following table compares the major sustainability reporting frameworks by their focus, scope, jurisdiction, application date, and whether they are mandatory or voluntary.

The next comparison focuses on the type of instrument, its geographic coverage, the topics addressed and definition of materiality.

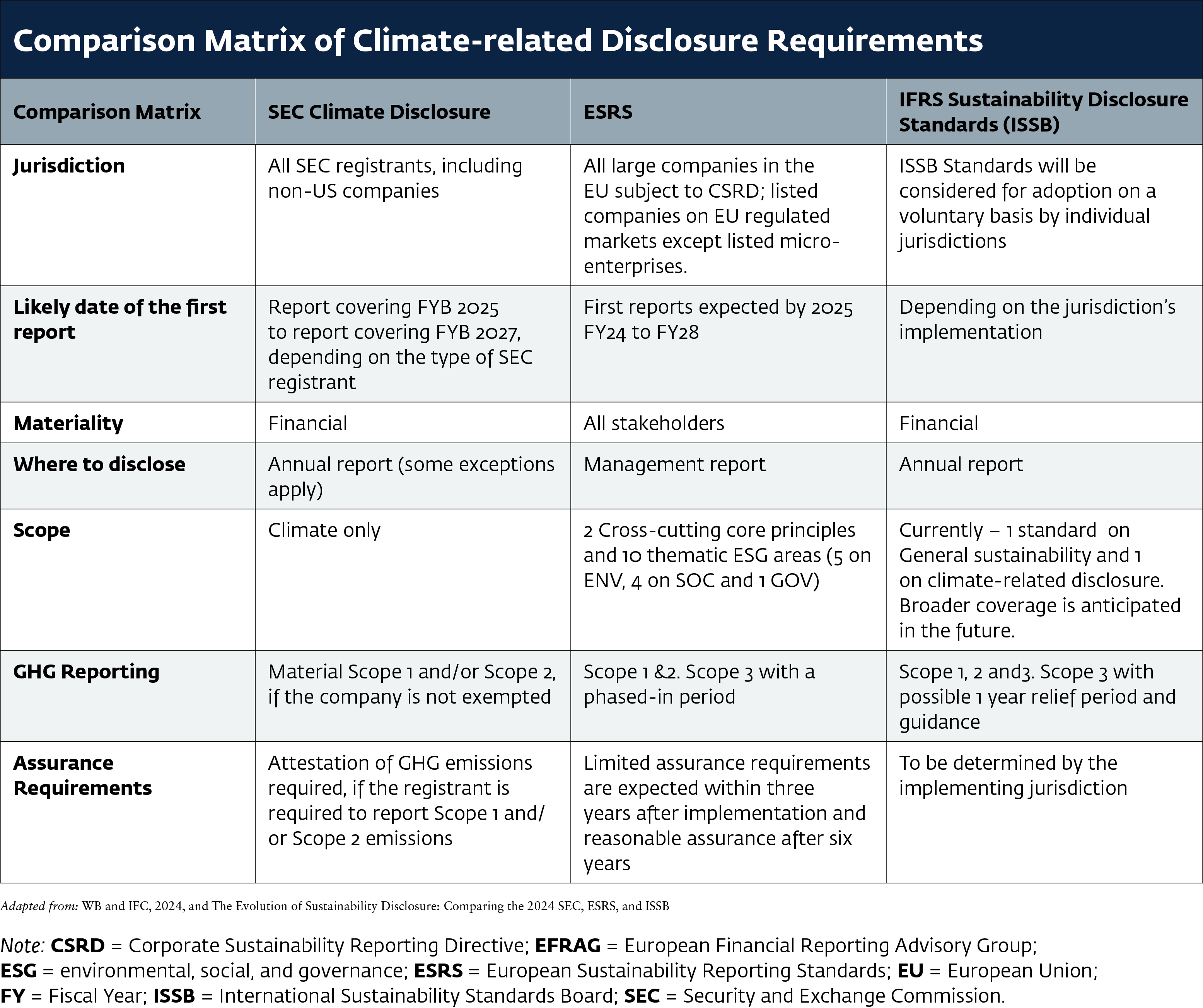

Comparing Sustainability Disclosure Requirements

Comparing US Securities and Exchange Commission (SEC), European Sustainability Reporting Standards (ESRS), and International Sustainability Standards Board (ISSB) Climate Disclosures.

Comparison studies used for the climate disclosure comparison table:

- The Evolution of Sustainability Disclosure: Comparing the 2022 SEC, ESRS, and ISSB Proposals;

- Draft European Sustainability Reporting Standards, Appendix V: IFRS Sustainability Standards and ESRS Reconciliation Table (ESRS E1 versus IFRS S2, pages 54–73);

- Comparison ISSB IFRS S2 Climate-Related Disclosures with the TCFD Recommendations;

- GRI and the European Sustainability Reporting Standards (ESRS): Q&A.

- The Enhancement and Standardization of Climate-Related Disclosures: Final Rules

- ESRS–ISSB Standards Interoperability Guidance

- IFRS Sustainability Disclosure Taxonomy 2024

- ESRS – TNFD Correspondence Mapping

- Interoperability mapping between the GRI Standards and the TNFD Recommended Disclosures and metrics

Further guidance: Implementation Guidance for the International Sustainability Standards Board (ISSB) Standards and the European Sustainability Reporting Standards (ESRS), (WBCSD CFO Network).

Developing a comprehensive solution for corporate sustainability reporting is complex. As a result, global organizations have frameworks, standards, and platforms that shape the landscape and guide the latest sustainability reporting.