Entendendo as estruturas de relatórios globais

Há um interesse crescente dos investidores em empresas envolvidas em atividades comerciais sustentáveis. Os investidores querem entender como as empresas lidam com questões como mudança climática, diversidade de gênero ou riscos da cadeia de suprimentos que possam ter um impacto material em seus negócios.

As bolsas de valores e os órgãos reguladores desenvolvem regulamentos de sustentabilidade e divulgação climática. Atualmente, 71 - mais da metade das bolsas de valores em todo o mundo têm orientações sobre divulgação de ESG; em 2015, eram apenas 13. Há regras obrigatórias em 27 mercados, dos quais 16 são mercados emergentes, de acordo com o banco de dados de Bolsas de Valores de Sustentabilidade da ONU.

A harmonização dos padrões de divulgação de sustentabilidade criará dados e divulgações de ESG confiáveis e comparáveis, o que é cada vez mais essencial para atrair capital e investidores e evitar o greenwashing.

Um passo positivo na convergência de diferentes padrões e estruturas são os novos padrões de sustentabilidade e relatórios climáticos da Fundação IFRS e dos Padrões Europeus de Relatórios de Sustentabilidade.

Os padrões de Divulgação de Sustentabilidade do IFRS foram finalizados em junho de 2023 e entraram em vigor a partir de janeiro de 2024, e os Padrões Europeus de Relatórios de Sustentabilidade foram lançados em julho de 2023, entrando em vigor a partir de janeiro de 2024.

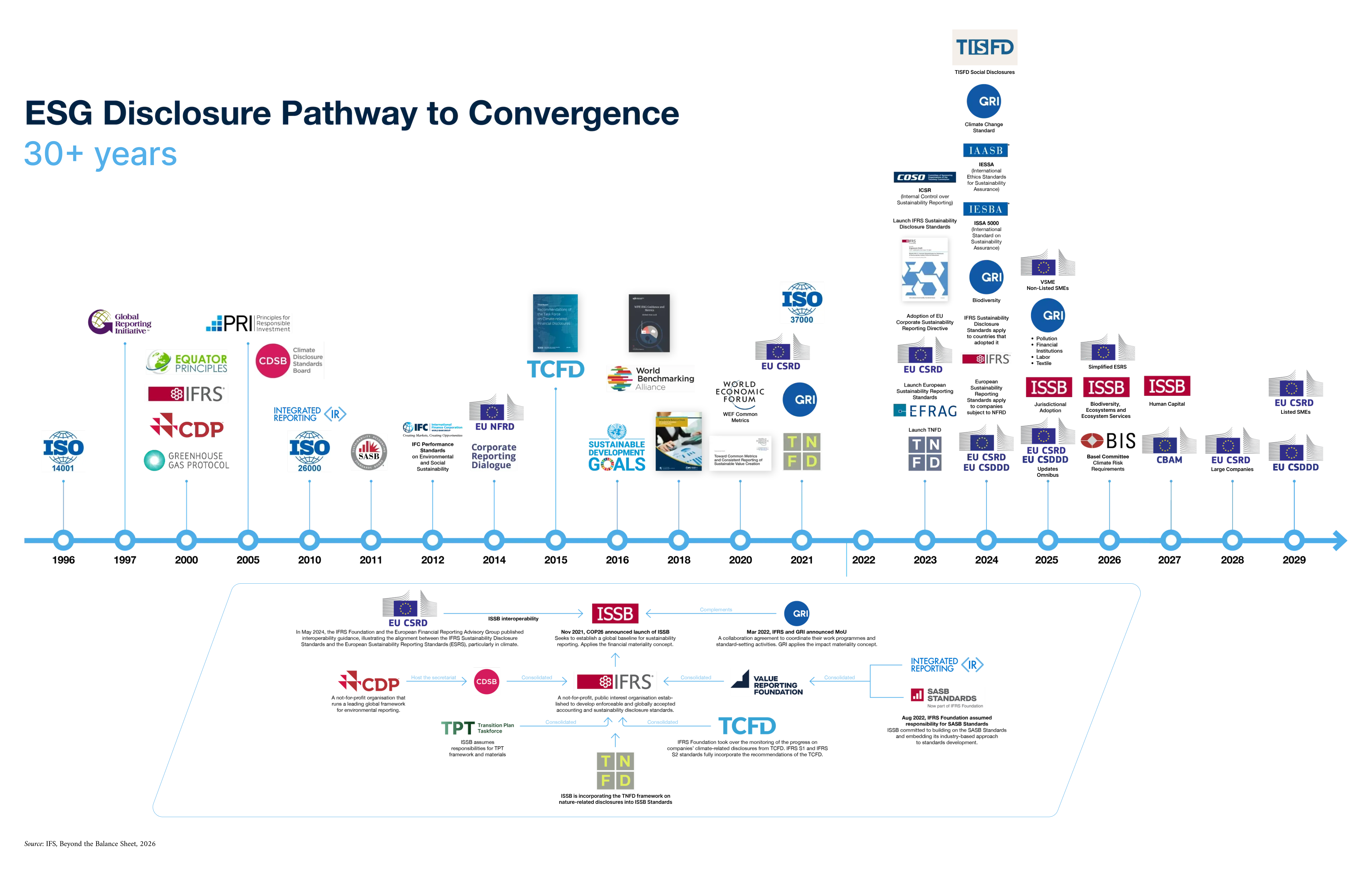

O diagrama abaixo apresenta os principais marcos da divulgação da sustentabilidade nos últimos 30 anos.

Source: IFC, 2025

-

Padrões de divulgação de sustentabilidade IFRS

As Normas de Divulgação de Sustentabilidade IFRS são desenvolvidas pelo International Sustainability Standards Board (ISSB). O ISSB é um órgão independente do setor privado que desenvolve - no interesse público - normas que resultarão em uma linha de base global abrangente e de alta qualidade de divulgações de sustentabilidade, com foco nas necessidades dos investidores e dos mercados financeiros.

As normas do ISSB se concentram nos riscos e oportunidades relacionados à sustentabilidade que são relevantes para os investidores e se baseiam, em grande parte, nas Recomendações da Força-Tarefa para Informações Financeiras Relacionadas ao Clima (TCFD) (veja abaixo). Dessa forma, a implementação das Normas de Divulgação de Sustentabilidade IFRS também significa que uma empresa implementou as Recomendações TCFD. As normas abrangem quatro áreas principais de conteúdo

- Governança: os processos de governança, controles e procedimentos que a entidade utiliza para monitorar e gerenciar riscos e oportunidades relacionados à sustentabilidade

- Estratégia: a abordagem que a entidade utiliza para gerenciar riscos e oportunidades relacionados à sustentabilidade

- Gestão de riscos: os processos que a organização utiliza para identificar, avaliar, priorizar e monitorar riscos e oportunidades relacionados à sustentabilidade

- Métricas e Metas: o desempenho da entidade em relação aos riscos e oportunidades relacionados à sustentabilidade, incluindo o progresso em direção a quaisquer metas que a entidade tenha estabelecido ou seja obrigada a cumprir por lei ou regulamento

A IFRS S1 Requisitos Gerais para a Divulgação de Informações Financeiras Relacionadas à Sustentabilidade fornece os fundamentos conceituais e o conteúdo de divulgação para relatar todas as informações financeiras relacionadas à sustentabilidade, enquanto a IFRS S2 Divulgações Relacionadas ao Clima fornece requisitos mais detalhados com foco nos riscos e oportunidades relacionados ao clima, dentro dos fundamentos da IFRS S1. As empresas devem considerar a aplicabilidade das normas do Sustainability Accounting Standards Board (SASB) baseadas no setor (veja abaixo) ao aplicar as Normas de Divulgação de Sustentabilidade do IFRS. As normas devem ser aplicadas a partir de 1º de janeiro de 2024.

Considerando que o IFRS S2 exige a divulgação de informações sobre planos de transição (quando uma entidade tiver esse plano) e que os planos de transição são um componente crescente das divulgações corporativas relacionadas ao clima, o ISSB anunciou que assumirá a responsabilidade pelos materiais específicos de divulgação desenvolvidos pela Força-Tarefa do Plano de Transição. Potencialmente baseado em iniciativas pré-existentes, incluindo os padrões da SASB, a orientação do CDSB e o trabalho da Força-Tarefa sobre Divulgações Financeiras Relacionadas à Natureza, o ISSB também decidiu analisar os riscos e oportunidades associados à biodiversidade e ao capital humano nos próximos dois anos.

Projetados para adoção obrigatória pelos órgãos reguladores, os Padrões de Divulgação de Sustentabilidade IFRS estão sendo implementados gradualmente nos requisitos de relatórios em todo o mundo.

-

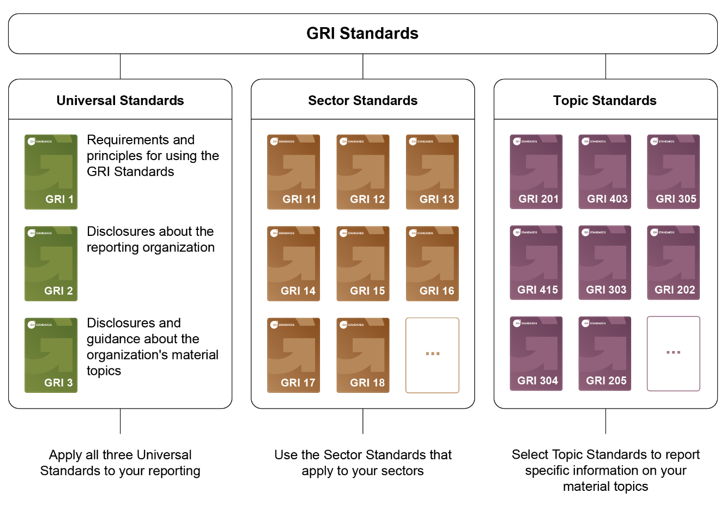

Padrões da Global Reporting Initiative (GRI)

Os Padrões GRI representam as melhores práticas globais para a elaboração de relatórios públicos sobre uma série de impactos econômicos, ambientais e sociais. Os relatórios de sustentabilidade baseados nos Padrões fornecem informações sobre as contribuições positivas ou negativas de uma organização para o desenvolvimento sustentável.

Os Padrões da GRI são um sistema modular de padrões interconectados, que fornecem uma visão abrangente dos tópicos materiais de uma organização, seus impactos relacionados e como eles são gerenciados. Três séries de padrões apóiam o processo de elaboração de relatórios:

- os Padrões Universais da GRI, que se aplicam a todas as organizações;

- os Padrões Setoriais da GRI, aplicáveis a setores específicos;

- os Padrões Temáticos da GRI, cada um listando as divulgações relevantes para um tópico específico.

O uso desses Padrões ajuda as organizações a determinar quais tópicos são mais importantes para alcançar o desenvolvimento sustentável.

Fonte: GRI">

-

Padrões europeus de relatórios de sustentabilidade

A Diretiva de Relatórios de Sustentabilidade Corporativa da UE (CSRD) moderniza e fortalece as regras relativas às informações sociais e ambientais que as empresas com sede na UE, ou aquelas com operações significativas na UE, devem relatar. Um conjunto mais amplo de grandes empresas, bem como PMEs listadas, agora será obrigado a relatar sobre sustentabilidade.

Certas empresas europeias precisam aplicar as novas regras a partir do exercício financeiro de 2024, para relatórios publicados em 2025, e outras terão que ser implementadas gradualmente em 2026 e 2027. Por fim, as empresas não pertencentes à UE com operações significativas na Europa terão que começar a relatar a partir de 2029, com base nos dados do ano fiscal de 2028, usando um conjunto simplificado de padrões.

As empresas sujeitas à CSRD terão de apresentar relatórios de acordo com os Padrões Europeus de Relatórios de Sustentabilidade (ESRS).

As ESRS estabelecem requisitos gerais para orientar a divulgação de todas as informações de sustentabilidade e exigem que todas as organizações relatem sobre quatro áreas de divulgações gerais:

- Governança

- Estratégia

- Impactos, riscos e oportunidades

- Métricas e metas

Dependendo de sua materialidade para a organização, ela também pode divulgar usando uma série de padrões tópicos:

Ambiental

- Mudanças climáticas

- Poluição

- Recursos hídricos e marinhos

- Biodiversidade e ecossistemas

- Uso de recursos e economia circular

Social

- Força de trabalho própria

- Trabalhadores da cadeia de valor

- Comunidades afetadas

- Consumidores e usuários finais

Governança

-

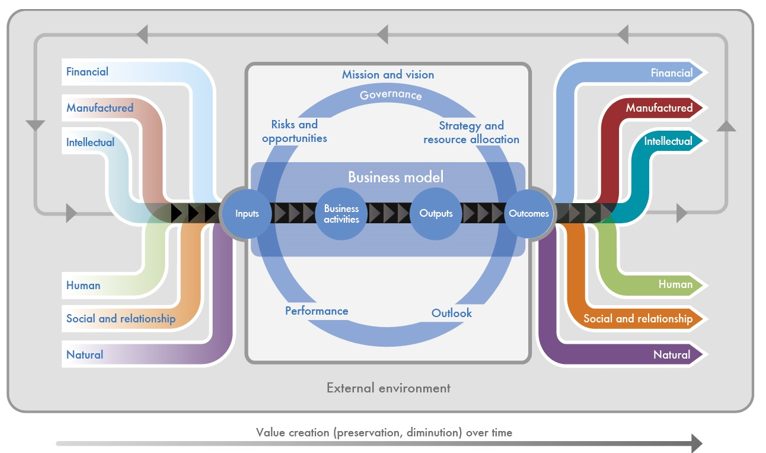

Estrutura de Relatórios Integrados (parte da Fundação IFRS)

A Estrutura de Relatórios Integrados é uma estrutura baseada em princípios usada pelas organizações para comunicar de forma clara e concisa como sua estratégia, governança, desempenho e perspectivas - no contexto de seu ambiente externo - levam à criação, preservação ou erosão de valor ao longo do tempo. A Estrutura de Relatórios Integrados categoriza as entradas e os resultados do acompanhamento em seis capitais: Financeiro, Manufaturado, Intelectual, Humano, Social e de Relacionamento, e Natural.

A partir de agosto de 2022, o International Sustainability Standards Board (ISSB) da IFRS Foundation assumiu a responsabilidade pela Estrutura de Relatórios Integrados.

-

Normas SASB (parte da Fundação IFRS)

Os Padrões SASB ajudam as empresas a divulgar informações relevantes de sustentabilidade específicas do setor para seus investidores no contexto dos Padrões de Divulgação de Sustentabilidade IFRS (ver acima).

Disponíveis para 77 setores, as Normas SASB identificam os riscos e as oportunidades relacionados à sustentabilidade com maior probabilidade de afetar os fluxos de caixa de uma entidade, o acesso a financiamento e o custo de capital a curto, médio ou longo prazo e os tópicos de divulgação e métricas com maior probabilidade de serem úteis aos investidores.

A partir de agosto de 2022, o International Sustainability Standards Board (ISSB) da IFRS Foundation assumiu a responsabilidade pelas Normas SASB. O ISSB se comprometeu a manter, aprimorar e desenvolver as Normas SASB e incentivar seu uso, e em 2023 atualizou as normas para garantir sua aplicabilidade internacional.

-

Regras de divulgação climática da SEC dos EUA

A Comissão de Valores Mobiliários dos EUA adotou novas regras sobre divulgações relacionadas ao clima em março de 2024. Essas regras se aplicam a todas as empresas que têm um requisito existente de reportar à SEC, incluindo empresas não americanas que negociam ações em uma bolsa de valores dos EUA.

Com base nas recomendações do TCFD (veja abaixo), as regras de divulgação exigirão que os registrantes da SEC divulguem informações sobre

- Riscos materiais relacionados ao clima

- Impactos materiais dos riscos relacionados ao clima na estratégia, no modelo de negócios e nas perspectivas da organização

- Quaisquer atividades de adaptação ou mitigação de riscos climáticos realizadas pelo registrante, se aplicável

- Uma descrição do plano de transição climática do registrante, se aplicável

- Os resultados materiais relacionados ao clima de uma análise de cenário, se aplicável

- O uso de um preço interno de carbono pelo registrante, se relevante

- Supervisão dos riscos relacionados ao clima pelo conselho de administração e pela gerência do registrante

- Processos de gerenciamento de riscos climáticos, se aplicável

- Metas e objetivos relacionados ao clima, se aplicáveis e relevantes

- Métricas materiais de emissões de Escopo 1 e/ou Escopo 2, se a empresa não estiver isenta

- Determinadas questões financeiras relacionadas ao risco climático materializado

A implementação em fases, com um subconjunto de registrantes obrigados a relatar um subconjunto das regras a partir do ano fiscal que começa em 2025, até a implementação completa para relatórios que abrangem o ano fiscal que começa em 2027

Um resumo dos requisitos está disponível aqui.

-

Recomendações da Força-Tarefa sobre Divulgações Financeiras Relacionadas ao Clima (TCFD) (parte da Fundação IFRS)

As recomendações da Força-Tarefa para Divulgação Financeira Relacionada ao Clima (TCFD) foram lançadas em 2017 "para ajudar a identificar as informações necessárias para que investidores, credores e subscritores de seguros avaliem e precifiquem adequadamente os riscos e oportunidades relacionados ao clima" As recomendações da TCFD são compostas por quatro elementos principais:

- Governança

- Estratégia

- Gerenciamento de riscos

- Métricas e metas

As recomendações foram concebidas para implementação voluntária, mas estão se tornando cada vez mais obrigatórias em mercados como Brasil, Japão, Cingapura, Suíça, Reino Unido e outros. Mais de 4.900 empresas forneceram relatórios TCFD em outubro de 2023.

O padrão de divulgação relacionado ao clima e à sustentabilidade geral do Conselho Internacional de Normas de Sustentabilidade (ISSB) marcou o ponto culminante do TCFD e o ISSB agora assumiu a responsabilidade de monitorar o progresso das divulgações relacionadas ao clima das empresas a partir do TCFD.

Para obter recursos adicionais sobre a TCFD, visite o TCFD Knowledge Hub, consulte o relatório de status final da TCFD e a página da web de publicações da TCFD.

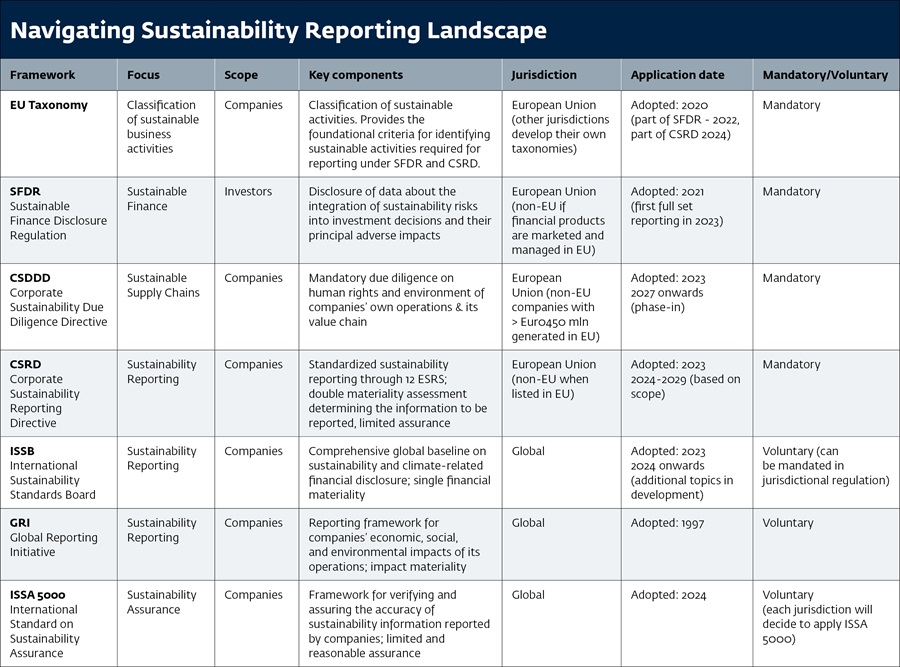

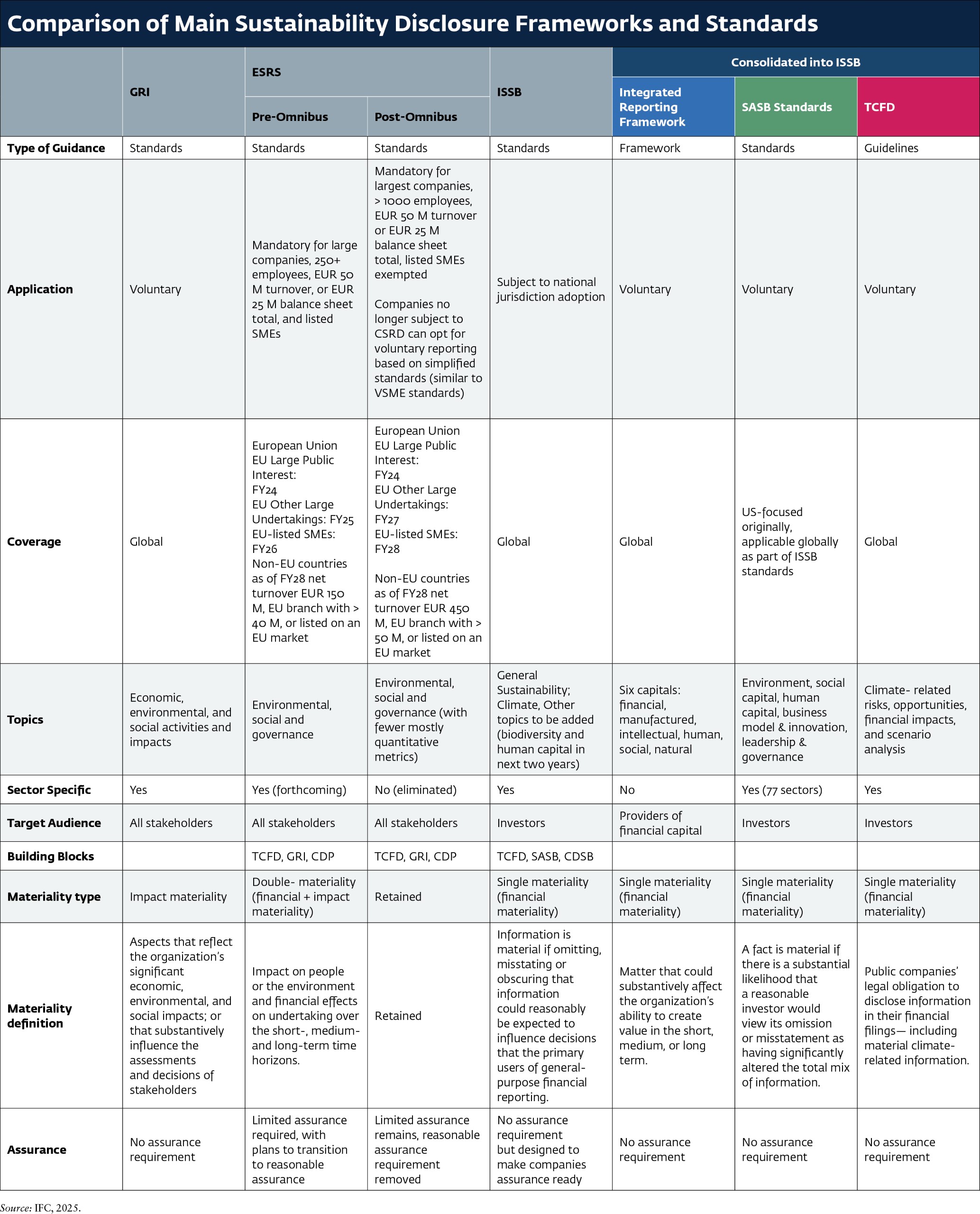

Comparação dos padrões e estruturas de relatórios de sustentabilidade

A tabela abaixo apresenta uma comparação resumida das principais estruturas e padrões de sustentabilidade, incluindo:

- International Sustainability Standards Board (ISSB) - IFRS S1 Requisitos Gerais para Divulgação de Informações Financeiras Relacionadas à Sustentabilidade e IFRS S2 Divulgações Relacionadas ao Clima;

- European Financial Reporting Advisory Group (EFRAG) - Normas Europeias para Relatórios de Sustentabilidade;

- Normas da Global Reporting Initiative (GRI);

- Estrutura de Relatórios Integrados - agora parte da Fundação IFRS;

- Sustainability Accounting Standards Board (SASB) - Normas SASB - Agora parte da IFRS Foundation;

- Recomendaçõesda Força-Tarefa sobre Divulgações Financeiras Relacionadas ao Clima (TCFD) - Agora parte da Fundação IFRS;

Para obter recursos sobre as Normas de Divulgação de Sustentabilidade IFRS, consulte o ISSB Knowledge Hub.

Para obter recursos sobre os Padrões Europeus de Relatórios de Sustentabilidade, consulte a Plataforma de Perguntas e Respostas do EFRAG ESRS.

A tabela a seguir compara as principais estruturas de relatórios de sustentabilidade por seu foco, escopo, jurisdição, data de aplicação e se são obrigatórias ou voluntárias.

A próxima comparação enfoca o tipo de instrumento, sua cobertura geográfica, os tópicos abordados e a definição de materialidade.

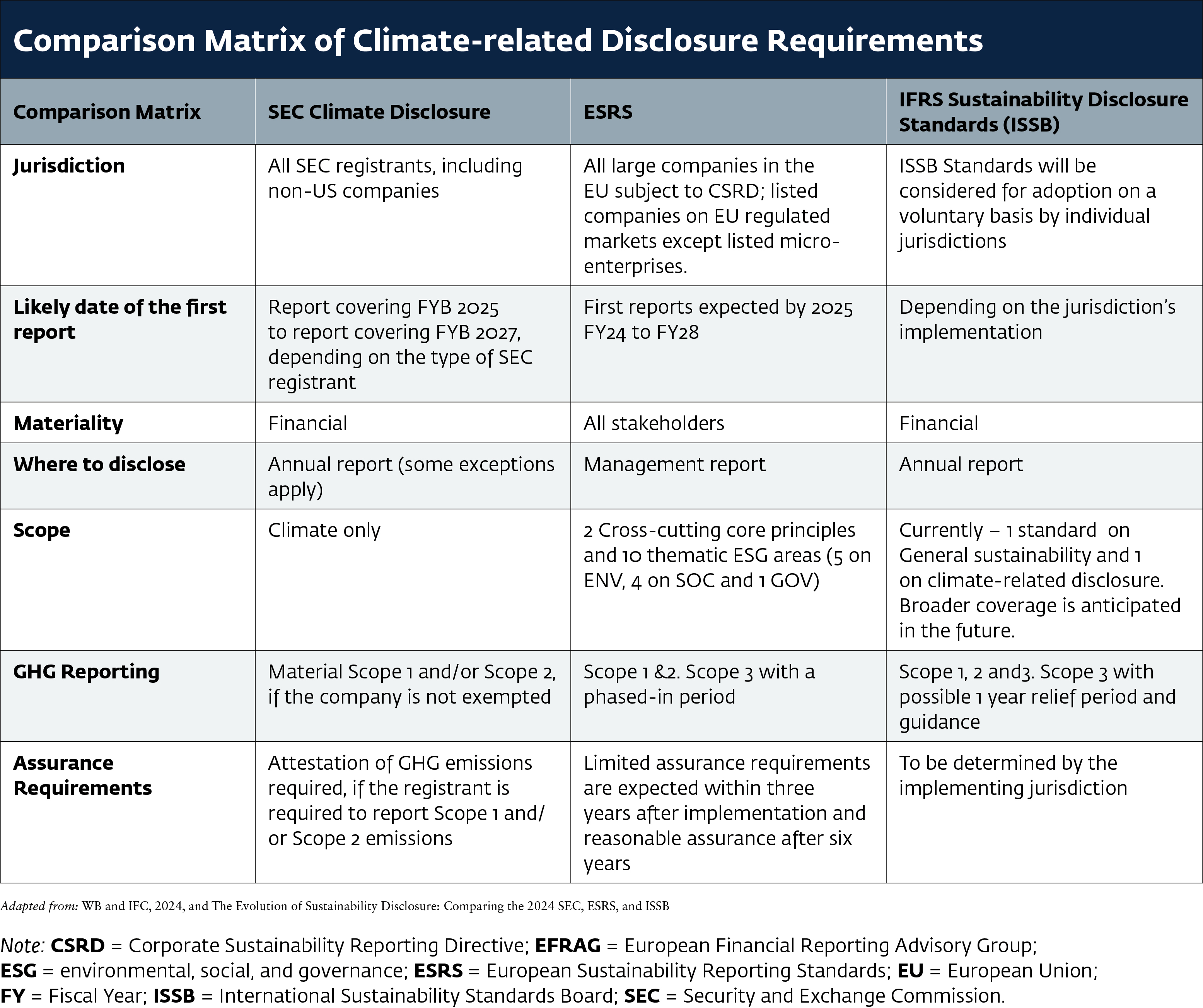

Comparação dos requisitos de divulgação de sustentabilidade

Comparação das divulgações climáticas da Comissão de Valores Mobiliários dos EUA (SEC), dos Padrões Europeus de Relatórios de Sustentabilidade (ESRS) e do Conselho Internacional de Padrões de Sustentabilidade (ISSB).

Source: WB and IFC, 2024, and The Evolution of Sustainability Disclosure: Comparing the 2024 SEC, ESRS, and ISSB Climate Disclosures">

Estudos de comparação usados para a tabela de comparação de divulgação climática:

- A evolução da divulgação de informações sobre sustentabilidade: Comparing the 2022 SEC, ESRS, and ISSB Proposals;

- Draft European Sustainability Reporting Standards, Apêndice V: IFRS Sustainability Standards and ESRS Reconciliation Table (ESRS E1 versus IFRS S2, páginas 54-73);

- Comparação das divulgações relacionadas ao clima da ISSB IFRS S2 com as recomendações da TCFD;

- GRI e os Padrões Europeus de Relatórios de Sustentabilidade (ESRS): PERGUNTAS E RESPOSTAS.

- O aprimoramento e a padronização das divulgações relacionadas ao clima: Regras finais

- Guia de interoperabilidade das normas ESRS-ISSB

- Taxonomia de divulgação de sustentabilidade do IFRS 2024

- Mapeamento de correspondência ESRS - TNFD

- Mapeamento de interoperabilidade entre os Padrões GRI e as Divulgações e métricas recomendadas pelo TNFD

Orientações adicionais: Guia de Implementação para as Normas do Conselho Internacional de Normas de Sustentabilidade (ISSB) e as Normas Europeias de Relatórios de Sustentabilidade (ESRS), (WBCSD CFO Network).

O desenvolvimento de uma solução abrangente para relatórios de sustentabilidade corporativa é complexo. Como resultado, as organizações globais têm estruturas, padrões e plataformas que moldam o cenário e orientam os mais recentes relatórios de sustentabilidade.