Comprendre les cadres de référence pour l'établissement des rapports mondiaux

Les investisseurs s'intéressent de plus en plus aux entreprises engagées dans des activités commerciales durables. Les investisseurs veulent comprendre comment les entreprises abordent des questions telles que le changement climatique, la diversité des genres ou les risques liés à la chaîne d'approvisionnement qui peuvent avoir un impact important sur leurs activités.

Les bourses et les autorités de régulation élaborent des réglementations en matière de développement durable et de divulgation d'informations sur le climat. À l'heure actuelle, 71 bourses - soit plus de la moitié - disposent de lignes directrices sur la publication d'informations ESG ; en 2015, elles n'étaient que 13. Des règles obligatoires existent dans 27 marchés, dont 16 sont des marchés émergents, selon la base de données UN Sustainability Stock Exchanges.

L'harmonisation des normes de divulgation en matière de développement durable permettra d'obtenir des données et des informations ESG fiables et comparables, ce qui est de plus en plus important pour attirer les capitaux et les investisseurs et empêcher l'écoblanchiment.

Les nouvelles normes d'information sur le développement durable et le climat de la Fondation IFRS et les normes européennes d'information sur le développement durable constituent une étape bienvenue dans la convergence des différentes normes et cadres.

Les normes IFRS de divulgation sur le développement durable ont été finalisées en juin 2023 et sont entrées en vigueur à partir de janvier 2024, et les normes européennes de reporting sur le développement durable ont été lancées en juillet 2023 et sont entrées en vigueur à partir de janvier 2024.

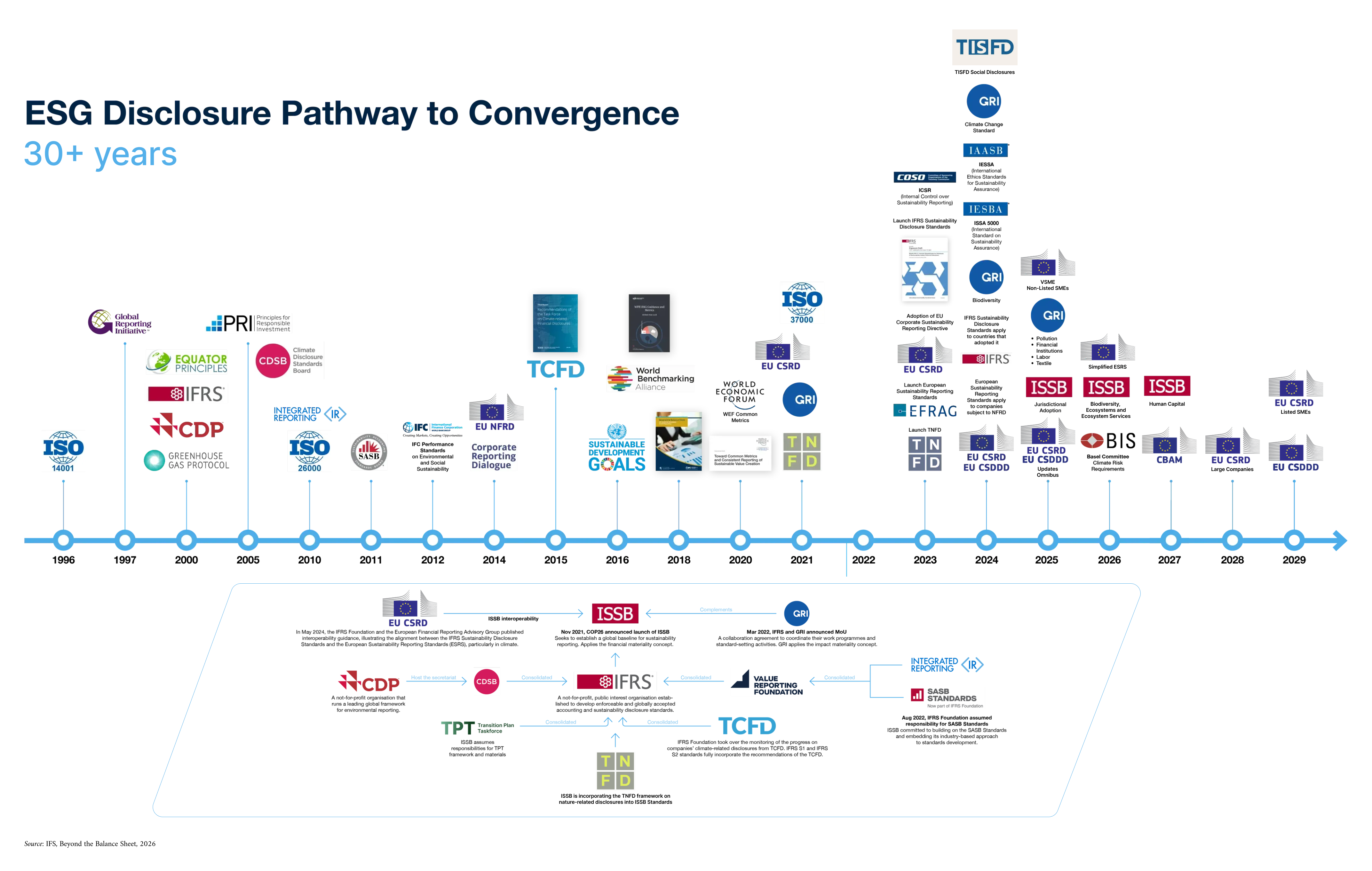

Le diagramme ci-dessous présente les principales étapes de la généralisation de la publication d'informations sur le développement durable au cours des 30 dernières années.

Source: IFC, 2025

-

Normes d'information sur le développement durable (IFRS)

Les normes IFRS relatives aux informations à fournir sur le développement durable sont élaborées par l'International Sustainability Standards Board (ISSB). L'ISSB est un organisme indépendant du secteur privé qui élabore, dans l'intérêt du public, des normes qui aboutiront à un référentiel mondial complet et de haute qualité en matière d'informations sur le développement durable, axé sur les besoins des investisseurs et des marchés financiers.

Les normes de l'ISSB se concentrent sur les risques et les opportunités liés au développement durable qui sont importants pour les investisseurs et s'appuient largement sur les recommandations de la Task Force for Climate-related Financial Information (TCFD ) (voir ci-dessous). Ainsi, la mise en œuvre des normes IFRS de divulgation sur le développement durable signifie également qu'une entreprise a mis en œuvre les recommandations de la TCFD. Les normes couvrent quatre domaines fondamentaux

- Gouvernance: les processus de gouvernance, les contrôles et les procédures que l'entité utilise pour surveiller et gérer les risques et les opportunités liés au développement durable

- Stratégie: l'approche utilisée par l'entité pour gérer les risques et les opportunités liés au développement durable

- Gestion des risques : les processus utilisés par l'entité pour identifier, évaluer, hiérarchiser et surveiller les risques et les opportunités liés au développement durable

- Mesures et objectifs: la performance de l'entité en ce qui concerne les risques et les opportunités liés au développement durable, y compris les progrès accomplis dans la réalisation des objectifs que l'entité a fixés ou qu'elle est tenue d'atteindre en vertu d'une loi ou d'une réglementation

L'IFRS S1 "General Requirements for Disclosure of Sustainability-Related Financial Information" fournit les bases conceptuelles et le contenu des informations à fournir pour la communication de toutes les informations financières liées au développement durable, tandis que l' IFRS S2 "Climate-Related Disclosures " fournit des exigences plus détaillées axées sur les risques et les opportunités liés au climat, dans le cadre des fondements de l'IFRS S1. Les entreprises doivent tenir compte de l'applicabilité des normes du Sustainability Accounting Standards Board (SASB) basées sur l'industrie (voir ci-dessous) lorsqu'elles appliquent les IFRS Sustainability Disclosure Standards. Ces normes doivent être appliquées à partir du 1er janvier 2024.

Étant donné que la norme IFRS S2 exige la publication d'informations sur les plans de transition (lorsqu'une entité dispose d'un tel plan) et que les plans de transition constituent un élément de plus en plus important des informations fournies par les entreprises sur le climat, l'ISSB a annoncé qu'il assumerait la responsabilité des documents d'information spécifiques élaborés par le groupe de travail sur les plans de transition. S'appuyant potentiellement sur des initiatives préexistantes, notamment les normes de la SASB, les orientations du CDSB et les travaux du groupe de travail sur les informations financières liées à la nature, l'ISSB a également décidé d'examiner les risques et les opportunités liés à la biodiversité et au capital humain au cours des deux prochaines années.

Conçues pour être adoptées obligatoirement par les autorités de réglementation, les normes IFRS de divulgation d'informations sur le développement durable sont progressivement mises en œuvre dans les obligations d'information partout dans le monde.

-

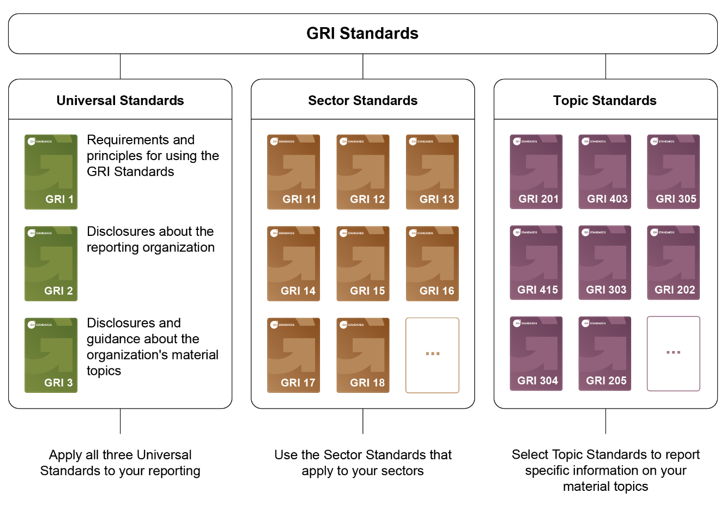

Normes de la Global Reporting Initiative (GRI)

Les normes de la GRI représentent les meilleures pratiques mondiales en matière de rapports publics sur une série d'impacts économiques, environnementaux et sociaux. Les rapports sur le développement durable fondés sur les normes fournissent des informations sur les contributions positives ou négatives d'une organisation au développement durable.

Les normes GRI sont un système modulaire de normes interconnectées, offrant une image complète des thèmes matériels d'une organisation, de leurs impacts et de la manière dont ils sont gérés. Trois séries de normes soutiennent le processus de reporting

- les normes universelles de la GRI, qui s'appliquent à toutes les organisations ;

- les normes sectorielles de la GRI, qui s'appliquent à des secteurs spécifiques

- les normes thématiques de la GRI, qui énumèrent chacune les informations à fournir sur un sujet particulier.

L'utilisation de ces normes aide les organisations à déterminer quels sont les sujets les plus propices au développement durable.

Source : GRI">

-

Normes européennes d'information sur le développement durable

La directive européenne sur les rapports de durabilité des entreprises (CSRD) modernise et renforce les règles concernant les informations sociales et environnementales que les entreprises ayant leur siège dans l'UE, ou celles ayant des activités significatives dans l'UE, doivent publier. Un plus grand nombre de grandes entreprises, ainsi que des PME cotées en bourse, seront désormais tenues d'établir des rapports sur le développement durable.

Certaines entreprises européennes doivent appliquer les nouvelles règles à partir de l'exercice 2024, pour les rapports publiés en 2025, les autres étant introduites progressivement en 2026 et 2027. Enfin, les entreprises non européennes qui exercent des activités significatives en Europe devront commencer à produire des rapports à partir de 2029, sur la base des données de l'exercice 2028, en utilisant un ensemble simplifié de normes.

Les entreprises soumises au CSRD devront établir leurs rapports conformément aux normes européennes de rapport sur le développement durable (ESRS).

Les ESRS fixent des exigences générales pour guider la divulgation de toutes les informations sur le développement durable et exigent que toutes les organisations fassent rapport sur quatre domaines d'informations générales:

- Gouvernance

- La stratégie

- Impacts, risques et opportunités

- Mesures et objectifs

En fonction de leur importance pour l'organisation, celle-ci peut également publier des informations sur la base d'un certain nombre de normes thématiques :

Environnement

- Changement climatique

- La pollution

- Eau et ressources marines

- Biodiversité et écosystèmes

- Utilisation des ressources et économie circulaire

Social

- Main d'œuvre propre

- Travailleurs de la chaîne de valeur

- Communautés affectées

- Consommateurs et utilisateurs finaux

Gouvernance

-

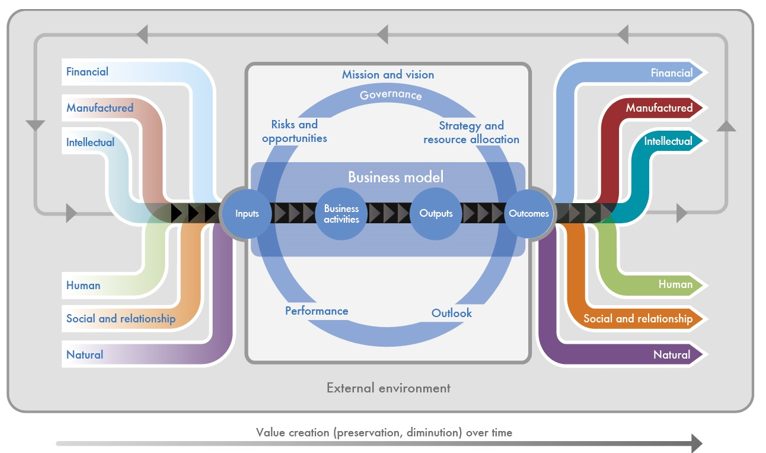

Cadre de référence pour les rapports intégrés (partie de la Fondation IFRS)

Le cadre du rapport intégré est un cadre fondé sur des principes utilisé par les organisations pour communiquer de manière claire et concise sur la manière dont leur stratégie, leur gouvernance, leurs performances et leurs perspectives - dans le contexte de leur environnement externe - conduisent à la création, à la préservation ou à l'érosion de la valeur au fil du temps. Le cadre du rapport intégré classe les intrants et les résultats de l'accompagnement en six catégories de capitaux : Financier, Industriel, Intellectuel, Humain, Social et relationnel, et Naturel.

Depuis août 2022, le Conseil international des normes de développement durable (ISSB) de la Fondation IFRS assume la responsabilité du cadre de référence pour l'établissement de rapports intégrés.

-

Normes SASB (partie de la Fondation IFRS)

Lesnormes de la SASB aident les entreprises à communiquer à leurs investisseurs des informations importantes sur le développement durable, spécifiques à leur secteur d'activité, dans le cadre des normes IFRS de divulgation d'informations sur le développement durable (voir ci-dessus).

Disponibles pour 77 secteurs d'activité, les normes SASB identifient les risques et opportunités liés au développement durable les plus susceptibles d'affecter les flux de trésorerie, l'accès au financement et le coût du capital d'une entité à court, moyen ou long terme, ainsi que les sujets d'information et les paramètres les plus susceptibles d'être utiles aux investisseurs.

Depuis août 2022, l'International Sustainability Standards Board (ISSB) de l'IFRS Foundation assume la responsabilité des normes SASB. L'ISSB s'est engagé à maintenir, améliorer et faire évoluer les normes SASB et à encourager leur utilisation, et en 2023, il a mis à jour les normes pour garantir leur applicabilité internationale.

-

Règles de la SEC en matière de divulgation d'informations sur le climat

La Securities and Exchange Commission (SEC) des États-Unis a adopté de nouvelles règles sur la divulgation d'informations liées au climat en mars 2024. Ces règles s'appliquent à toutes les entreprises qui ont l'obligation de faire rapport à la SEC, y compris les entreprises non américaines qui négocient des actions sur une bourse américaine.

Fondées sur les recommandations de la TCFD (voir ci-dessous), les règles de divulgation exigeront des entreprises enregistrées auprès de la SEC qu'elles divulguent des informations sur les points suivants

- Les risques importants liés au climat

- Les incidences importantes des risques liés au climat sur la stratégie, le modèle d'entreprise et les perspectives de l'organisation

- Toute activité d'atténuation ou d'adaptation au risque climatique entreprise par le déclarant, le cas échéant

- Une description du plan de transition climatique du déclarant, le cas échéant

- Les résultats importants d'une analyse de scénarios liés au climat, le cas échéant

- L'utilisation d'un prix interne du carbone par le déclarant, le cas échéant

- La surveillance des risques liés au climat par le conseil d'administration et la direction du déclarant

- Les processus de gestion des risques climatiques, le cas échéant

- Les cibles et objectifs liés au climat, s'il y a lieu et s'ils sont importants

- Mesures importantes des émissions de portée 1 et/ou de portée 2, si l'entreprise n'est pas exemptée

- Certaines questions financières liées au risque climatique matérialisé

La mise en œuvre progressive, avec un sous-ensemble de déclarants tenus de déclarer un sous-ensemble de règles à partir de leur exercice commençant en 2025, jusqu'à la mise en œuvre complète pour les rapports couvrant l'exercice commençant en 2027

Un résumé des exigences est disponible ici.

-

Recommandations du groupe de travail sur les informations financières liées au climat (TCFD) (partie de la Fondation IFRS)

Les recommandations de la Task Force for Climate-Related Financial Disclosure (TCFD ) ont été lancées en 2017 "pour aider à identifier les informations dont ont besoin les investisseurs, les prêteurs et les souscripteurs d'assurance pour évaluer et tarifer de manière appropriée les risques et les opportunités liés au climat" Les recommandations de la TCFD comprennent quatre éléments fondamentaux :

- Gouvernance

- La stratégie

- Gestion des risques

- Mesures et objectifs

Les recommandations étaient destinées à une mise en œuvre volontaire, mais elles deviennent de plus en plus obligatoires sur des marchés tels que le Brésil, le Japon, Singapour, la Suisse, le Royaume-Uni et d'autres. Plus de 4 900 entreprises ont fourni des rapports de la TCFD en octobre 2023.

La norme de divulgation liée au climat et à la durabilité générale de l'International Sustainability Standards Board (ISSB) a marqué l'aboutissement de la TCFD et l'ISSB a maintenant pris la responsabilité de suivre les progrès des divulgations liées au climat des entreprises de la TCFD.

Pour des ressources supplémentaires sur la TCFD, visitez le Knowledge Hub de la TCFD, consultez le rapport final sur l'état d'avancement de la TCFD et la page web des publications de la TCFD.

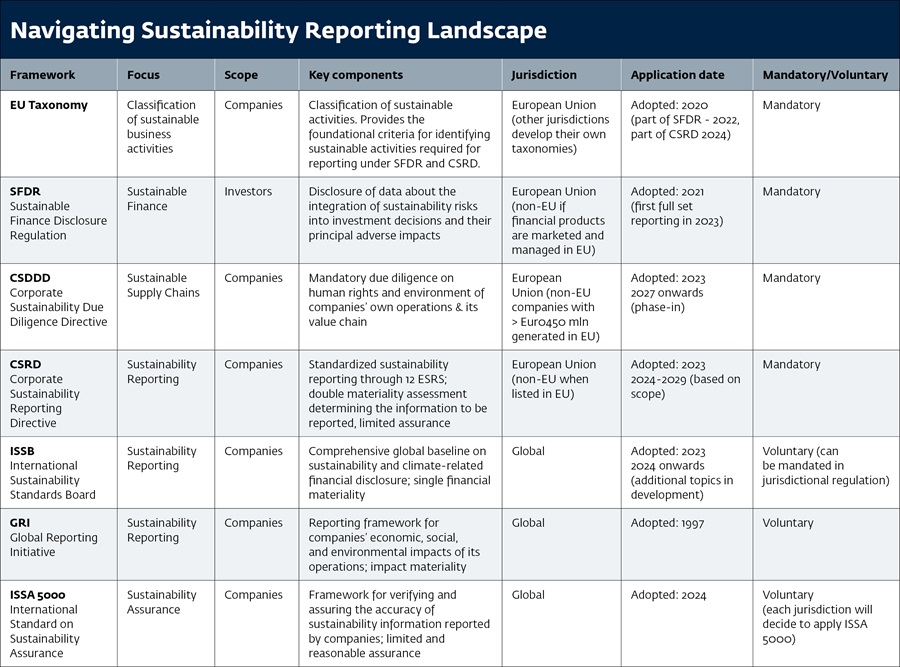

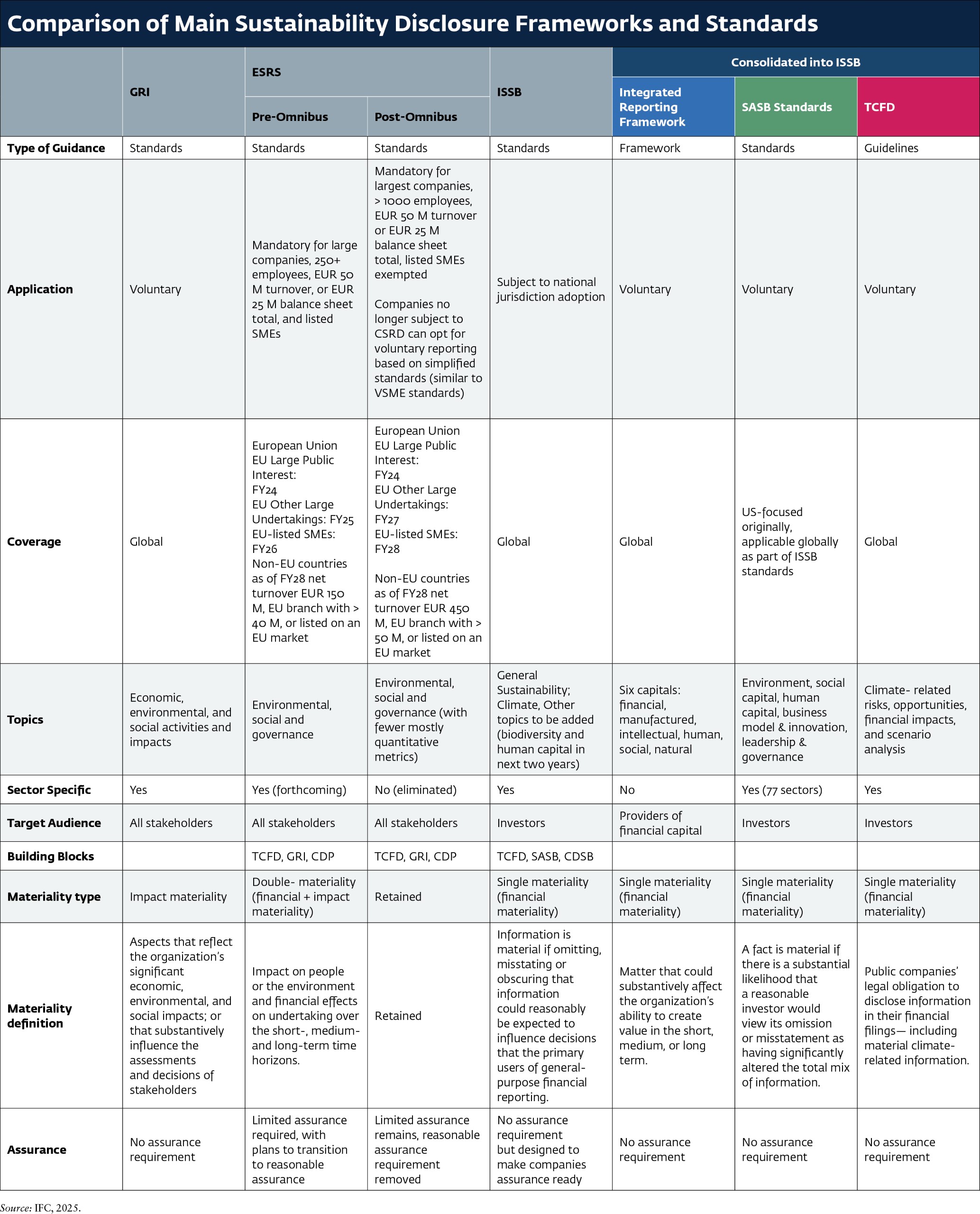

Comparaison des normes et cadres de reporting en matière de développement durable

Le tableau ci-dessous présente une comparaison sommaire des principaux cadres et normes en matière de développement durable :

- International Sustainability Standards Board (ISSB ) - IFRS S1 General Requirements for Disclosure of Sustainability-Related Financial Information et IFRS S2 Climate-related Disclosures;

- Groupe consultatif pour l'information financière en Europe (EFRAG ) - Normes européennes d'information sur le développement durable;

- Normes de la Global Reporting Initiative (GRI);

- Integrated Reporting Framework - fait désormais partie de l'IFRS Foundation ;

- Sustainability Accounting Standards Board (SASB ) - Normes SASB - Fait maintenant partie de la Fondation IFRS ;

- Recommandations duTask Force on Climate-related Financial Disclosures (TCFD) - Fait maintenant partie de l'IFRS Foundation ;

Pour des ressources sur les IFRS Sustainability Disclosure Standards, consultez le Knowledge Hub de l'ISSB.

Pour des ressources sur les normes européennes d'information sur le développement durable, consultez la plateforme EFRAG ESRS Q&A.

Le tableau suivant compare les principaux cadres d'information sur le développement durable en fonction de leur objectif, de leur portée, de leur juridiction, de leur date d'application et de leur caractère obligatoire ou volontaire.

La comparaison suivante porte sur le type d'instrument, sa couverture géographique, les thèmes abordés et la définition de la matérialité.

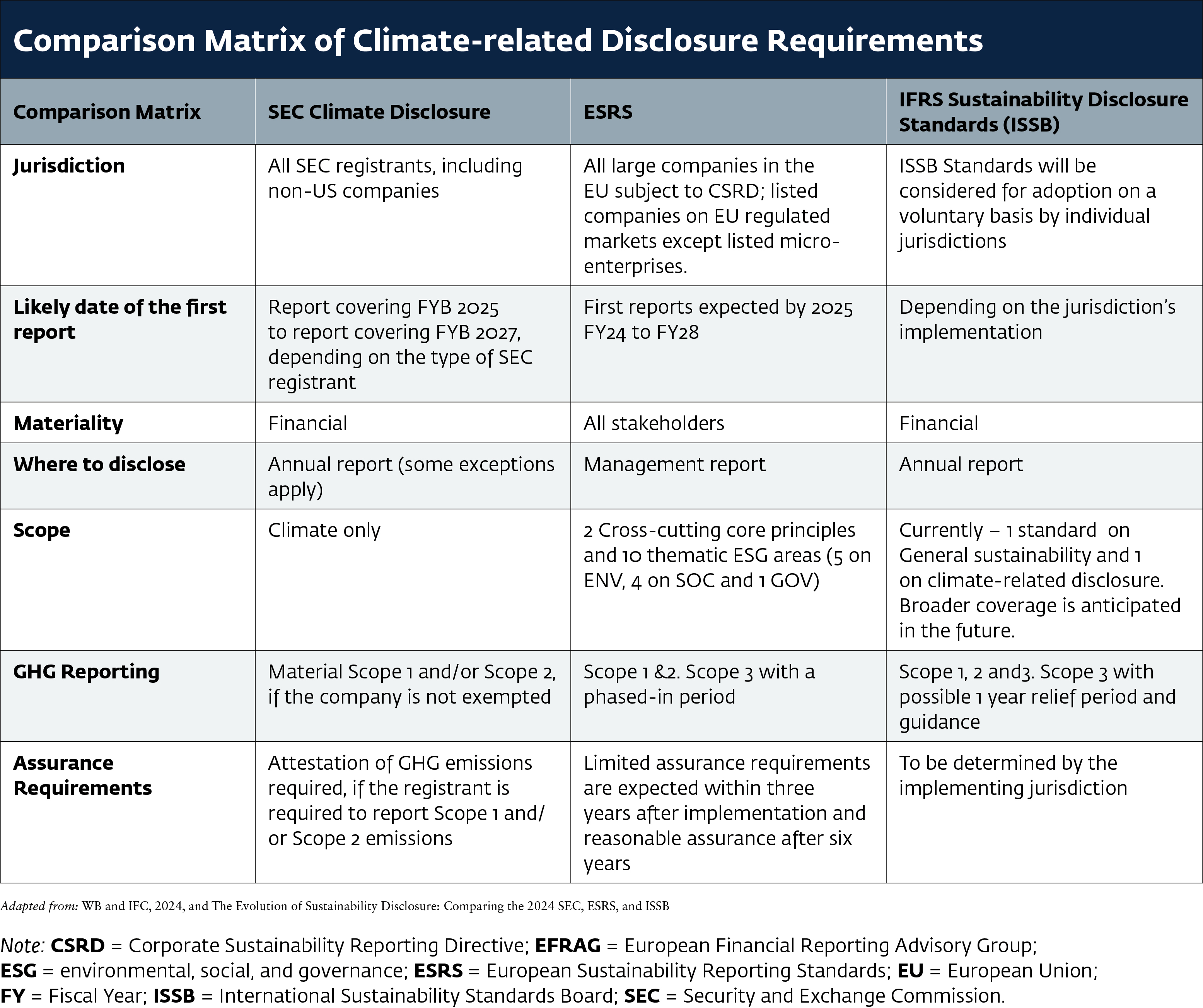

Comparaison des obligations d'information en matière de développement durable

Comparaison des informations sur le climat de la Securities and Exchange Commission (SEC) des États-Unis, des normes européennes de reporting sur le développement durable (ESRS) et de l'International Sustainability Standards Board (ISSB).

Source: WB and IFC, 2024, and The Evolution of Sustainability Disclosure: Comparing the 2024 SEC, ESRS, and ISSB Climate Disclosures">

Études comparatives utilisées pour le tableau de comparaison des informations sur le climat :

- L'évolution de la divulgation en matière de développement durable : Comparaison des propositions de la SEC, de l'ESRS et de l'ISSB pour 2022;

- Projet de normes européennes d'information sur le développement durable, annexe V : tableau de réconciliation entre les normes IFRS sur le développement durable et les normes ESRS (ESRS E1 versus IFRS S2, pages 54-73) ;

- Comparaison de l'ISSB IFRS S2 Climate-Related Disclosures avec les recommandations de la TCFD;

- La GRI et les normes européennes de reporting sur le développement durable (ESRS) : Q&R.

- L'amélioration et la normalisation des informations relatives au climat : Règles finales

- Directives sur l'interopérabilité des normes ESRS-ISSB

- Taxonomie IFRS sur les informations à fournir en matière de développement durable 2024

- Correspondance ESRS - TNFD

- Correspondance d'interopérabilité entre les normes GRI et les informations et mesures recommandées par le TNFD

Plus d'informations : Implementation Guidance for the International Sustainability Standards Board (ISSB) Standards and the European Sustainability Reporting Standards (ESRS), (WBCSD CFO Network).

L'élaboration d'une solution complète pour les rapports sur le développement durable des entreprises est complexe. C'est pourquoi les organisations internationales disposent de cadres, de normes et de plateformes qui façonnent le paysage et guident les derniers rapports sur le développement durable.