Entender los Marcos Mundiales de Información

Existe un creciente interés de los inversores por las empresas que realizan actividades empresariales sostenibles. Los inversores quieren saber cómo abordan las empresas cuestiones como el cambio climático, la diversidad de género o los riesgos de la cadena de suministro que pueden tener un impacto material en su negocio.

Las bolsas y los reguladores desarrollan normativas de divulgación sobre sostenibilidad y clima. En la actualidad, 71 -más de la mitad de las bolsas de valores de todo el mundo- cuentan con orientaciones sobre divulgación de información ASG; en 2015, solo eran 13. Existen normas obligatorias en 27 mercados, de los cuales 16 son mercados emergentes, según la base de datos de Bolsas de Valores Sostenibles de la ONU.

La armonización de las normas de divulgación de la sostenibilidad creará datos y divulgaciones ESG fiables y comparables, lo que es cada vez más crítico para atraer capital e inversores y evitar el lavado verde.

Un paso positivo en la convergencia de diferentes normas y marcos son las nuevas normas de información sobre sostenibilidad y clima de la Fundación NIIF y las Normas Europeas de Información sobre Sostenibilidad.

Las normas de divulgación de la sostenibilidad de las NIIF se finalizaron en junio de 2023 y entraron en vigor a partir de enero de 2024, y las Normas Europeas de Información sobre la Sostenibilidad se lanzaron en julio de 2023 y entraron en vigor a partir de enero de 2024.

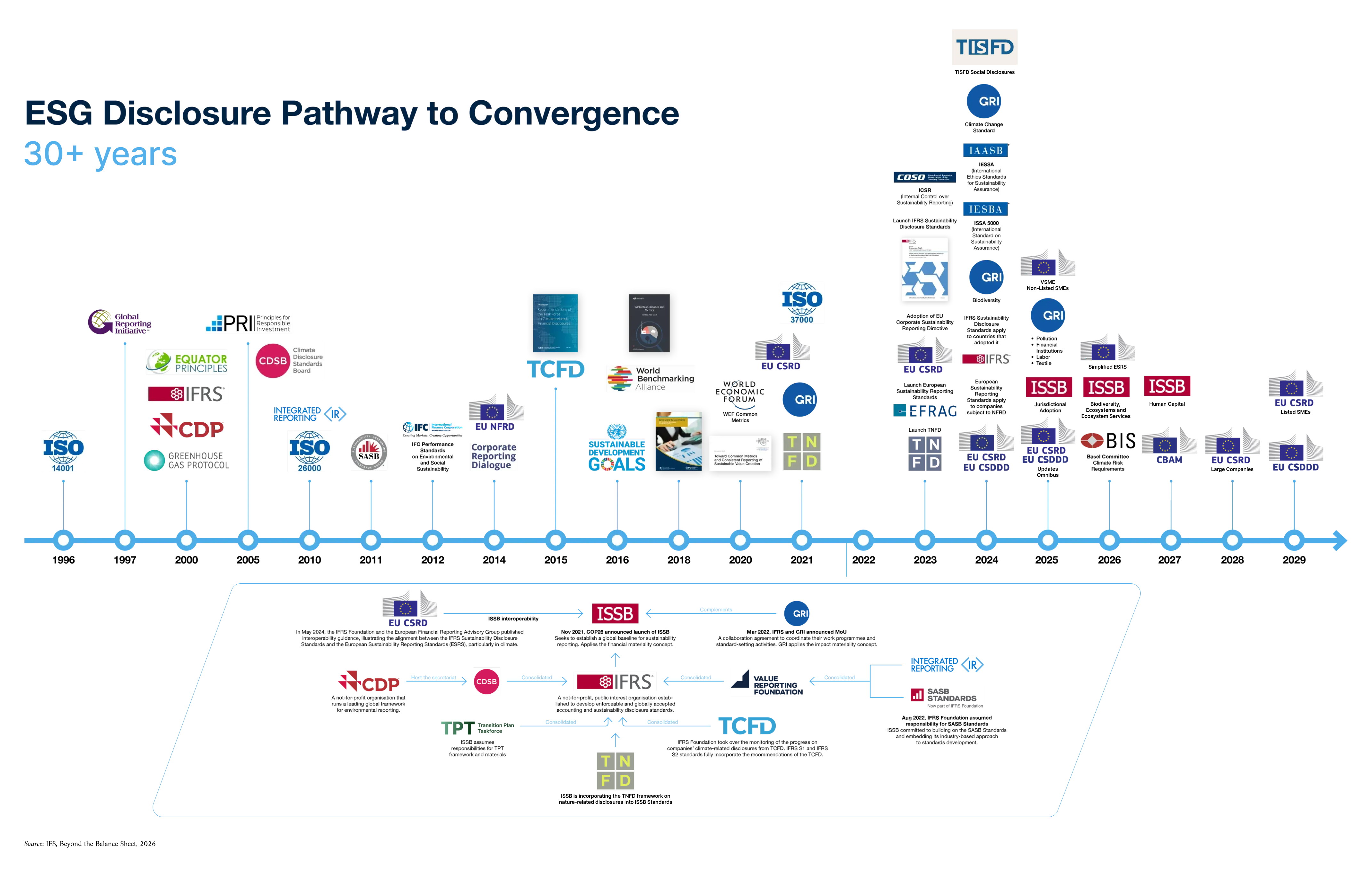

El diagrama que figura a continuación presenta los principales hitos de la divulgación de información sobre sostenibilidad en los últimos 30 años.

Source: IFC, 2025

-

NIIF Normas de divulgación de la sostenibilidad

El Consejo de Normas Internacionales de Sostenibilidad (ISSB) elabora las Normas NIIF de Divulgación de Información sobre Sostenibilidad. El ISSB es un organismo independiente del sector privado que elabora, en aras del interés público, normas que darán lugar a una base global de divulgación de la sostenibilidad de alta calidad y exhaustiva, centrada en las necesidades de los inversores y los mercados financieros.

Las normas de la ISSB se centran en los riesgos y oportunidades relacionados con la sostenibilidad que son importantes para los inversores y se basan en gran medida en las recomendaciones del Grupo de Trabajo sobre Información Financiera relacionada con el Clima (TCFD ) (véase más adelante). Como tal, la aplicación de las Normas NIIF de Divulgación de la Sostenibilidad también significa que una empresa ha aplicado las Recomendaciones del TCFD. Las normas abarcan cuatro áreas principales

- Gobernanza: los procesos de gobernanza, controles y procedimientos que la entidad utiliza para supervisar y gestionar los riesgos y oportunidades relacionados con la sostenibilidad

- Estrategia: el enfoque que utiliza la entidad para gestionar los riesgos y oportunidades relacionados con la sostenibilidad

- Gestión de riesgos: los procesos que utiliza la entidad para identificar, evaluar, priorizar y supervisar los riesgos y oportunidades relacionados con la sostenibilidad

- Métricas y objetivos: el rendimiento de la entidad en relación con los riesgos y oportunidades relacionados con la sostenibilidad, incluido el progreso hacia cualquier objetivo que la entidad se haya fijado o esté obligada a cumplir por ley o reglamento

La NIIF S1Requisitos generales para la divulgación de información financiera relacionada con la sostenibilidad proporciona los fundamentos conceptuales y el contenido de la divulgación para informar sobre toda la información financiera relacionada con la sostenibilidad, mientras que la NIIF S2 Divulgación de información relacionada con el clima proporciona requisitos más detallados centrados en los riesgos y oportunidades relacionados con el clima, dentro de los fundamentos de la NIIF S1. Las empresas deben tener en cuenta la aplicabilidad de las normas del Consejo de Normas Contables de Sostenibilidad (SASB) basadas en la industria (véase más adelante) al aplicar las normas de divulgación de la sostenibilidad de las NIIF. Las normas deberán aplicarse a partir del 1 de enero de 2024.

Dado que la NIIF S2 exige que se revele información sobre los planes de transición (cuando una entidad cuenta con un plan de este tipo) y que los planes de transición son un componente cada vez más importante de las revelaciones corporativas relacionadas con el clima, el ISSB anunció que asumirá la responsabilidad de los materiales específicos de revelación desarrollados por el Grupo de Trabajo del Plan de Transición. Basándose potencialmente en iniciativas preexistentes, como las normas de la SASB, las orientaciones de la CDSB y la labor del Grupo de trabajo sobre divulgación de información financiera relacionada con la naturaleza, la ISSB también decidió estudiar en los próximos dos años los riesgos y oportunidades asociados a la biodiversidad y el capital humano.

Diseñadas para su adopción obligatoria por los reguladores, las Normas de Divulgación de la Sostenibilidad de las NIIF se están implantando gradualmente en los requisitos de información de todo el mundo.

-

Normas de la Global Reporting Initiative (GRI)

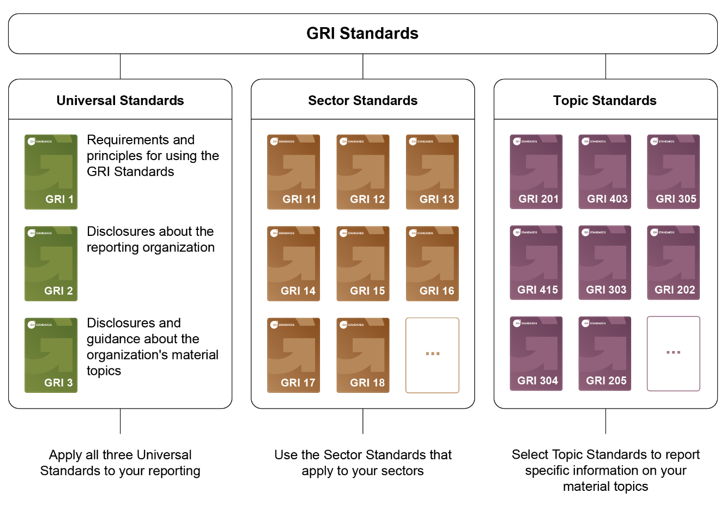

Los Estándares GRI representan las mejores prácticas mundiales para informar públicamente sobre una serie de impactos económicos, medioambientales y sociales. Los informes de sostenibilidad basados en los Estándares proporcionan información sobre las contribuciones positivas o negativas de una organización al desarrollo sostenible.

Los Estándares GRI son un sistema modular de estándares interconectados que ofrecen una visión global de los temas materiales de una organización, sus impactos relacionados y cómo se gestionan. El proceso de elaboración de informes se apoya en tres series de Estándares

- los Estándares Universales GRI, que se aplican a todas las organizaciones;

- los Estándares Sectoriales GRI, aplicables a sectores específicos;

- los Estándares Temáticos de GRI, cada uno de los cuales enumera la información relativa a un tema concreto.

El uso de estos Estándares ayuda a las organizaciones a determinar qué temas son los más adecuados para lograr un desarrollo sostenible.

Fuente: GRI">

-

Normas europeas para la elaboración de memorias de sostenibilidad

La Directiva de la UE sobre informes de sostenibilidad de las empresas moderniza y refuerza las normas relativas a la información social y medioambiental que deben comunicar las empresas con sede en la UE o con operaciones significativas en ella. Un conjunto más amplio de grandes empresas, así como las PYME que cotizan en bolsa, estarán ahora obligadas a informar sobre sostenibilidad.

Algunas empresas europeas tienen que aplicar las nuevas normas a partir del ejercicio 2024, para los informes publicados en 2025, y otras se irán incorporando progresivamente a lo largo de 2026 y 2027. Por último, las empresas no pertenecientes a la UE con operaciones significativas en Europa tendrán que empezar a informar a partir de 2029, sobre la base de los datos del ejercicio 2028, utilizando un conjunto simplificado de normas.

Las empresas sujetas al CSRD tendrán que informar de acuerdo con las Normas Europeas de Información sobre Sostenibilidad (ESRS).

Las NISR establecen requisitos generales para orientar la divulgación de toda la información sobre sostenibilidad y obligan a todas las organizaciones a informar sobre cuatro áreas de divulgación general:

- Gobernanza

- Estrategia

- Impactos, riesgos y oportunidades

- Métricas y objetivos

En función de su importancia para la organización, ésta también puede divulgar información utilizando una serie de normas temáticas:

Medio ambiente

- Cambio climático

- Contaminación

- Agua y recursos marinos

- Biodiversidad y ecosistemas

- Uso de los recursos y economía circular

Social

- Mano de obra propia

- Trabajadores de la cadena de valor

- Comunidades afectadas

- Consumidores y usuarios finales

Gobernanza

-

Marco Integrado de Elaboración de Informes (parte de la Fundación IFRS)

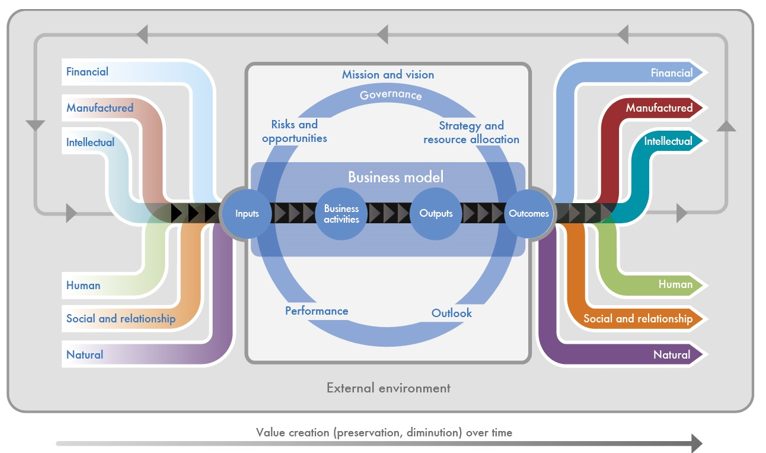

El Marco del Informe Integrado es un marco basado en principios que utilizan las organizaciones para comunicar de forma clara y concisa cómo su estrategia, gobernanza, rendimiento y perspectivas -en el contexto de su entorno externo- conducen a la creación, preservación o erosión de valor a lo largo del tiempo. El Marco de Informes Integrados clasifica los insumos y resultados de acompañamiento en seis capitales: Financiero, Industrial, Intelectual, Humano, Social y relacional, y Natural.

A partir de agosto de 2022, el Consejo de Normas Internacionales de Sostenibilidad (ISSB) de la Fundación IFRS asumió la responsabilidad del Marco de Información Integrada.

-

Normas SASB (parte de la Fundación IFRS)

Las normas dela SASB ayudan a las empresas a revelar a sus inversores información sustancial sobre sostenibilidad específica de su sector en el contexto de las normas de revelación de información sobre sostenibilidad de las NIIF (véase más arriba).

Disponibles para 77 sectores, las Normas SASB identifican los riesgos y oportunidades relacionados con la sostenibilidad que tienen más probabilidades de afectar a los flujos de efectivo, el acceso a la financiación y el coste del capital de una entidad a corto, medio o largo plazo, así como los temas de divulgación y las métricas que tienen más probabilidades de ser útiles para los inversores.

A partir de agosto de 2022, el Consejo de Normas Internacionales de Sostenibilidad (ISSB) de la Fundación NIIF asumió la responsabilidad de las Normas SASB. El ISSB se ha comprometido a mantener, mejorar y hacer evolucionar las Normas SASB y a fomentar su uso, y en 2023 actualizó las normas para garantizar su aplicabilidad internacional.

-

Normas de divulgación sobre el clima de la SEC de EE.UU

La Comisión del Mercado de Valores de EE.UU. ha adoptado nuevas normas sobre divulgación de información relacionada con el clima en marzo de 2024. Estas normas se aplican a todas las empresas que tienen la obligación de informar a la SEC, incluidas las empresas no estadounidenses que cotizan en bolsa en Estados Unidos.

Basadas en las recomendaciones del TCFD (véase más abajo), las normas de divulgación exigirán a las empresas registradas en la SEC que divulguen información sobre:

- Riesgos importantes relacionados con el clima

- Repercusiones importantes de los riesgos climáticos en la estrategia, el modelo empresarial y las perspectivas de la organización

- Cualquier actividad de mitigación o adaptación al riesgo climático emprendida por el registrante, si procede

- Una descripción del plan de transición climática del registrante, si procede

- Los resultados materiales relacionados con el clima de un análisis de escenarios, si procede

- El uso de un precio interno del carbono por parte del registrante, si procede

- Supervisión de los riesgos relacionados con el clima por parte del consejo de administración y la dirección del registrante

- Procesos de gestión de riesgos climáticos, si procede

- Metas y objetivos relacionados con el clima, si son aplicables y materiales

- Métricas de emisiones materiales de Alcance 1 y/o Alcance 2, si la empresa no está exenta

- Ciertos asuntos financieros relacionados con el riesgo climático materializado

La aplicación gradual, con un subconjunto de registrantes obligados a informar sobre un subconjunto de las normas a partir de su ejercicio fiscal que comienza en 2025, hasta la plena aplicación para los informes que cubren el ejercicio fiscal que comienza en 2027

Un resumen de los requisitos está disponible aquí.

-

Recomendaciones del Grupo de Trabajo sobre Información Financiera Relacionada con el Clima (TCFD) (parte de la Fundación IFRS)

Las recomendaciones del Grupo de Trabajo para la Divulgación Financiera Relacionada con el Clima (TCFD, por sus siglas en inglés) se lanzaron en 2017 "para ayudar a identificar la información que necesitan los inversores, prestamistas y suscriptores de seguros para evaluar y valorar adecuadamente los riesgos y oportunidades relacionados con el clima." Las recomendaciones de la TCFD constan de cuatro elementos básicos:

- Gobernanza

- Estrategia

- Gestión de riesgos

- Métricas y objetivos

Las recomendaciones se concibieron para su aplicación voluntaria, pero cada vez son más obligatorias en mercados como Brasil, Japón, Singapur, Suiza y Reino Unido, entre otros. Hasta octubre de 2023, más de 4.900 empresas habían presentado informes TCFD.

La norma de divulgación relacionada con el clima y la sostenibilidad general del Consejo Internacional de Normas de Sostenibilidad (ISSB) ) marcó la culminación del TCFD y el ISSB ha asumido ahora la responsabilidad de supervisar el progreso de las divulgaciones relacionadas con el clima de las empresas del TCFD.

Para obtener recursos adicionales sobre la TCFD, visite el Centro de conocimientos de la TCFD, consulte el informe final de situación de la TCFD y la página web de publicaciones de la TCFD.

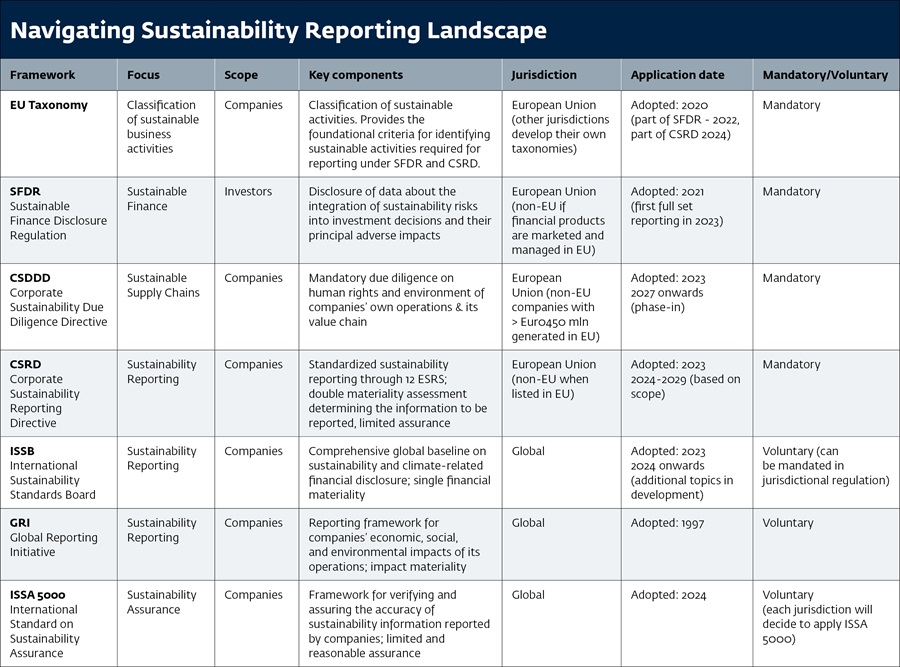

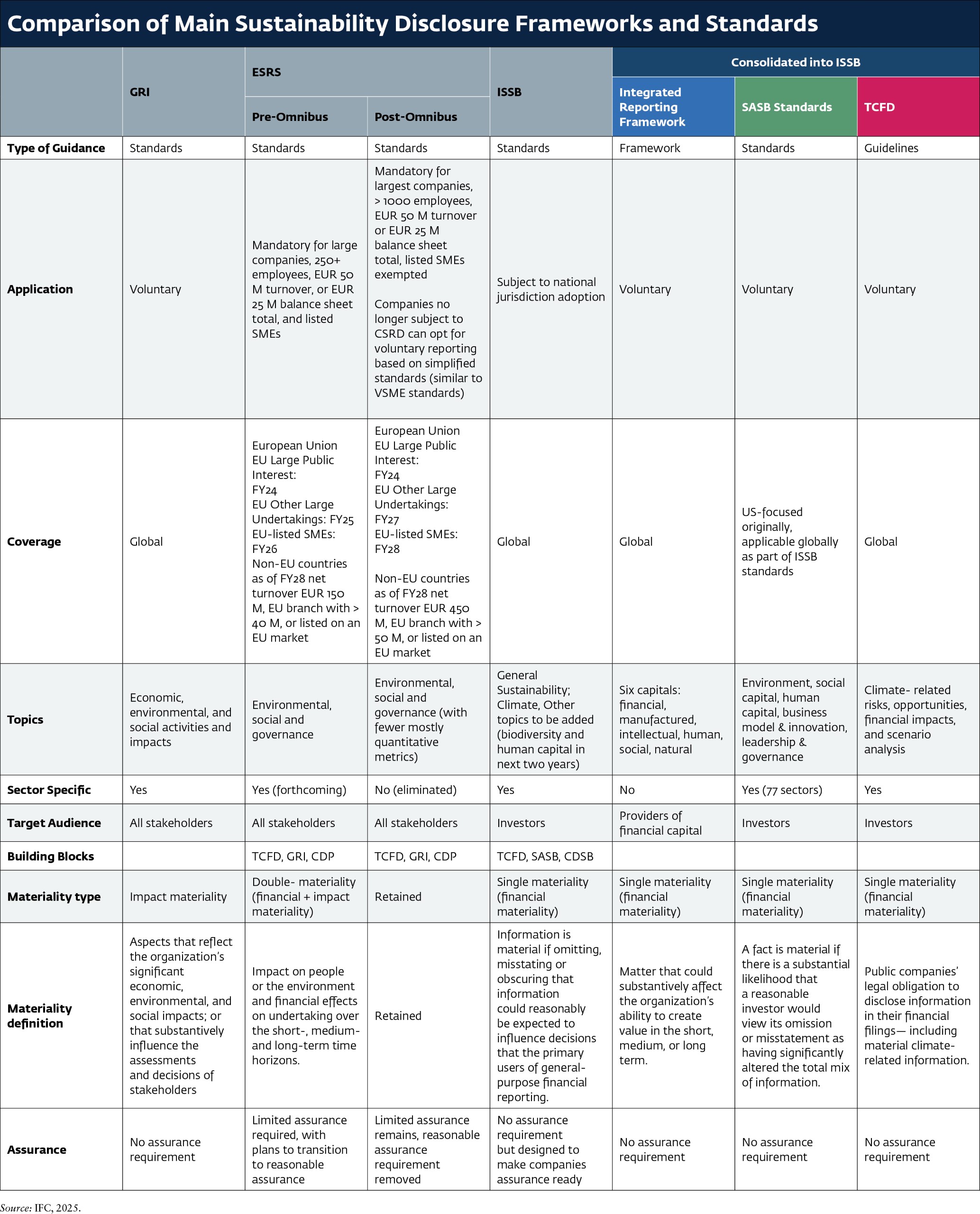

Comparación de normas y marcos de información sobre sostenibilidad

La tabla siguiente ofrece una comparación resumida de los principales marcos y normas de sostenibilidad, entre los que se incluyen:

- International Sustainability Standards Board (ISSB) - IFRS S1 General Requirements for Disclosure of Sustainability-Related Financial Information e IFRS S2 Climate-related Disclosures;

- Grupo Consultivo Europeo en materia de Información Financiera (EFRAG ) - Normas europeas de información sobre sostenibilidad;

- Normas de la Iniciativa Global de Informes (GRI);

- Marco Integrado de Elaboración de Informes - Ahora parte de la Fundación IFRS;

- Sustainability Accounting Standards Board (SASB) - Normas SASB - Ahora parte de la IFRS Foundation;

- Task Force on Climate-related Financial Disclosures (TCFD) Recommendations - Ahora parte de la IFRS Foundation;

Para recursos sobre las Normas NIIF para la divulgación de información sobre sostenibilidad, consulte el Centro de conocimientos de la ISSB.

Para recursos sobre las Normas Europeas de Información sobre Sostenibilidad, consulte la Plataforma EFRAG ESRS Q&A.

En la siguiente tabla se comparan los principales marcos para la elaboración de memorias de sostenibilidad en función de su enfoque, alcance, jurisdicción, fecha de aplicación y carácter obligatorio o voluntario.

La siguiente comparación se centra en el tipo de instrumento, su cobertura geográfica, los temas abordados y la definición de materialidad.

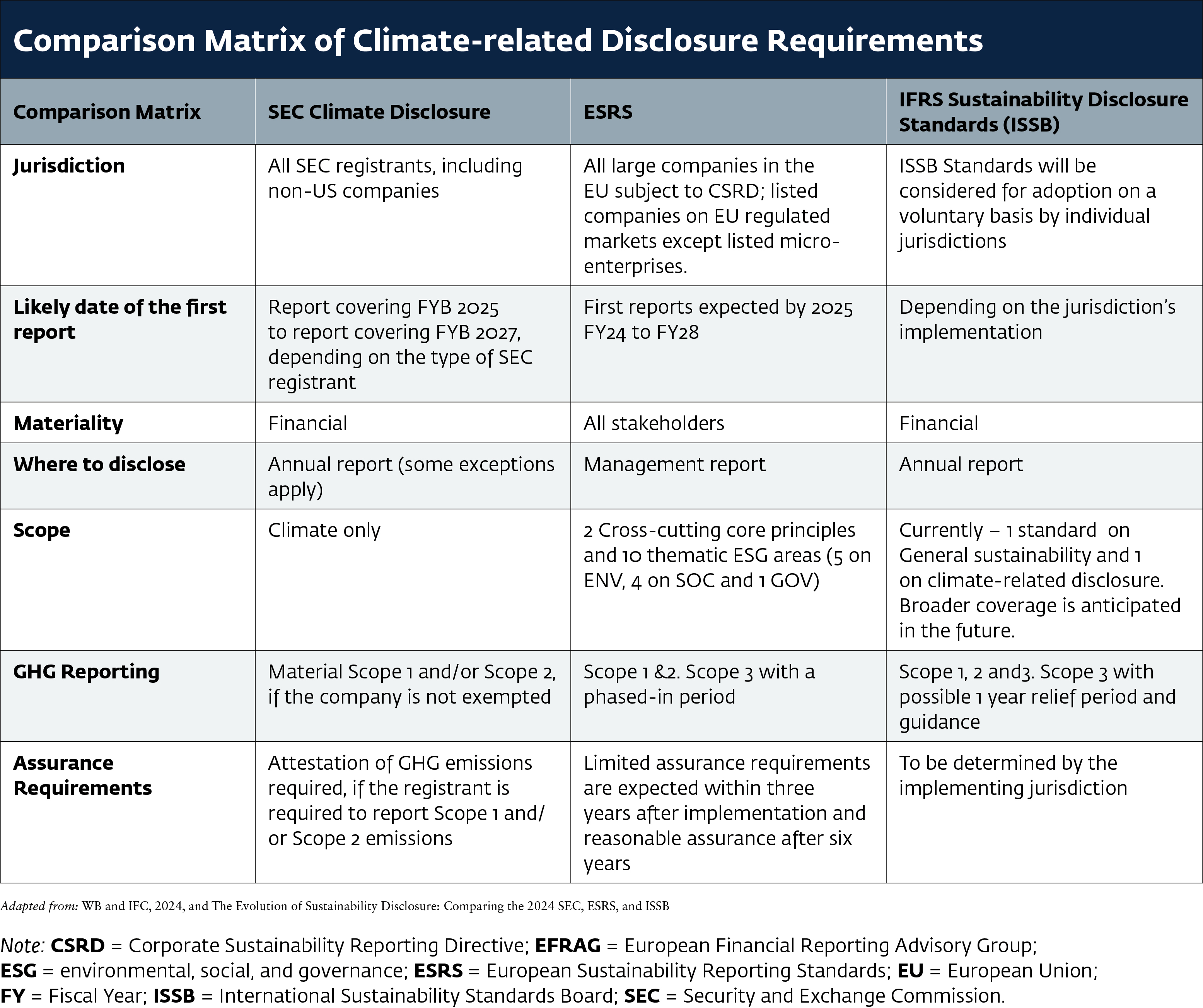

Comparación de los requisitos de información sobre sostenibilidad

Comparación de la información sobre el clima de la Comisión del Mercado de Valores de EE.UU. (SEC), las Normas Europeas de Información sobre Sostenibilidad (ESRS) y la Junta Internacional de Normas de Sostenibilidad (ISSB).

Source: WB and IFC, 2024, and The Evolution of Sustainability Disclosure: Comparing the 2024 SEC, ESRS, and ISSB Climate Disclosures">

Estudios comparativos utilizados para la tabla comparativa de divulgación climática:

- Evolución de la información sobre sostenibilidad: Comparing the 2022 SEC, ESRS, and ISSB Proposals;

- Borrador de las Normas Europeas para la Elaboración de Informes de Sostenibilidad, Apéndice V: Normas de sostenibilidad NIIF y tabla de conciliación N IIF (NIIF E1 frente a NIIF S2, páginas 54-73);

- Comparación ISSB IFRS S2 Climate-Related Disclosures con las Recomendaciones TCFD;

- GRI y las Normas Europeas para la Elaboración de Informes de Sostenibilidad (ESRS): Q&A.

- Mejora y normalización de la información relacionada con el clima: Normas finales

- Guía de interoperabilidad de las normas ESRS-ISSB

- Taxonomía de divulgación de la sostenibilidad de las NIIF 2024

- Correspondencia ESRS - TNFD

- Mapeo de interoperabilidad entre las Normas GRI y las Divulgaciones y métricas recomendadas del TNFD

Más información: Implementation Guidance for the International Sustainability Standards Board (ISSB) Standards and the European Sustainability Reporting Standards (ESRS), (WBCSD CFO Network).

El desarrollo de una solución integral para la elaboración de informes de sostenibilidad corporativa es complejo. Por ello, las organizaciones mundiales cuentan con marcos, normas y plataformas que configuran el panorama y orientan los últimos informes de sostenibilidad.